Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Glenn Purves – Global Head of Macro and Tuan Huynh – Chief Investment Strategist for Germany, Austria, Switzerland and Eastern Europe all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Higher-for-longer : U.S. tariffs and Europe boosting fiscal stimulus reinforce our view of policy rates staying higher versus pre-pandemic levels. We go underweight euro area bonds.

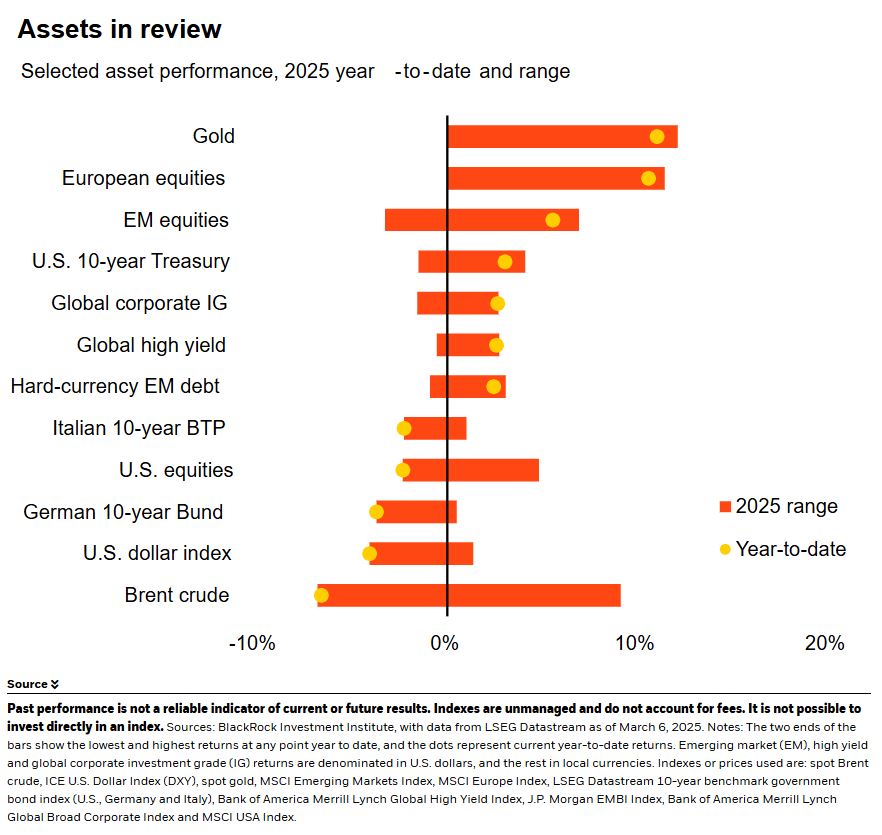

Market backdrop : U.S. stocks slid 3% last week on market concerns about policy uncertainty. German bond yields jumped the most since 1990 on big fiscal spending plans.

Week ahead : We think solid, if slowing, job growth and persistent wage pressures should show sticky core inflation in next week’s February U.S. CPI data.

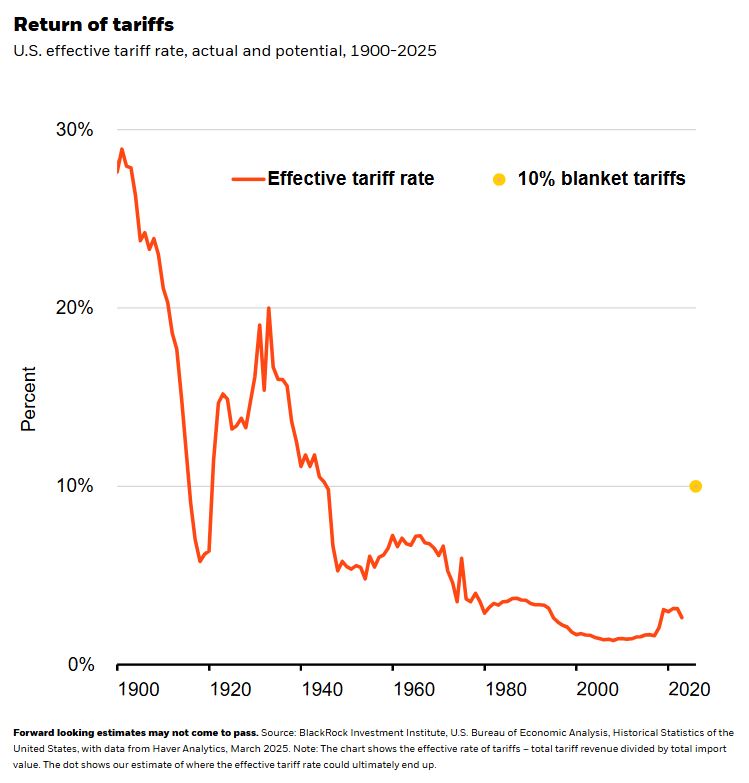

The U.S. briefly rolled out the largest tariffs in nearly a century on March 4: 25% tariffs on most Canadian and Mexican imports and an extra 10% on China. While most North American tariffs were later put on ice for another month, we think an average effective tariff rate of about 10% could be the eventual landing zone – with volatility along the way. See the chart. What matters more for near-term growth: any pain due to elevated uncertainty, including a potential U.S. government shutdown. Markets expect weaker U.S. growth to push the Fed to cut policy rates as in a typical business cycle. Yet we see a tough trade-off between supporting growth and curbing sticky inflation, limiting how much the Fed can cut. That reinforces our expectation of rates above pre-pandemic levels and higher bond yields. Germany’s plans for big defense and infrastructure spending mark a major fiscal policy shift.

Our scenarios framework – mapping potential outcomes for different mixes of growth, inflation and policy responses – helps us navigate this evolving market and economic landscape. In the past few weeks, markets have been increasingly pricing in a potential recession. We disagree. Why? Job creation has slowed slightly but the labor market remains strong in contrast to soft survey data showing declining consumer confidence. U.S. corporate earnings are also holding up. We still think earnings strength can broaden out beyond tech and to other regions as the buildout and adoption of artificial intelligence progresses. While heightened policy uncertainty will drive near-term market volatility, these other drivers keep us overweight U.S. stocks.

Bond yields can climb

Long-term U.S. Treasuries have rallied as recession fears grip markets. Yet they don’t reliably buffer against equity selloffs given persistent inflation. And yields could spike suddenly. One reason: Higher-for-longer Fed policy rates and persistently large fiscal deficits – even with tariff revenue and spending cuts – could push investors to demand more compensation for the risk of holding long-term bonds. We stay underweight long-term Treasuries, preferring short-term notes for income.

This pressure on yields is global. German bunds suffered their sharpest selloff since 1990 after the parties set to lead Germany’s next government agreed to a €500 billion infrastructure fund and axed deficit limits on defense spending. These plans – to be voted in parliament next week – come as the U.S. says Europe is no longer a top security priority. The European Union also proposed amending its budget rules to up defense spending. Europe could face higher-for-longer rates like the U.S. as greater government borrowing and spending stoke inflation. Plus, the European Central Bank is nearing the end of rate cuts. That’s all why we think euro area sovereign bond yields can rise further and go underweight. We trim our underweight to Japanese government bonds: yields have surged to 16-year highs. Yet we still see room for JGB yields to keep rising in a world of elevated debt levels and higher inflation.

Our bottom line

U.S. tariffs and Europe’s plans for a fiscal boost reinforce our expectation of higher-for-longer interest rates and bond yields. We go underweight euro area bonds. Policy uncertainty could keep weighing on U.S. stocks near term.Market backdrop

The S&P 500 slid 3% last week, its biggest weekly drop in six months and dragging the index into negative territory for the year. Ten-year U.S. Treasury yields were flat on the week but about 50 basis points below the year’s high, while 10-year German bund yields jumped about 45 basis points last week – the largest surge since German reunification in 1990. U.S. payrolls data showing slower but still solid job gains suggests market concerns about a recession are overdone, in our view.We’re focusing on the U.S. CPI for February out this week. We expect inflation pressures to remain elevated given strong job growth and persistent wage pressures that suggest core inflation will stay above the Fed’s 2% policy target. Now U.S. tariffs could potentially boost inflation pressures depending on their scope and implementation. We think that makes the Fed unlikely to cut interest rates as much as markets are pricing in.

Week ahead

March 10 : Japan trade balance

March 12 : U.S. CPI; Japan corporate goods

March 13 : U.S. PPI

March 14 : U.S. University of Michigan sentiment survey; UK GDP

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 12th March, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.