Coming out of the depths of the pandemic, US equity and fixed income markets are facing new challenges this year amidst a rising interest rate environment and deceleration in growth. With this changing backdrop, Franklin Templeton Investment Solutions’ Ed Perks shares his latest outlook and the investment opportunities he sees across asset classes.

Key Points:

- The US equity and fixed income markets are facing challenges due to a slowing US economy along with a significant pivot in monetary policy towards a more hawkish stance.

- Combating inflation has become a priority, and investor focus has shifted towards the uncertain impact of rising interest rates on the economy and markets.

- Despite challenges, US corporations are faring well so far in 2022, and the strength of the US labour market could delay or prevent a US recession.

Equity and Fixed Income Markets Facing Challenges

Looking back to the latter part of 2021, the US market environment was robust for equities, with strong economic growth that led to stock valuations that appeared appropriate to us. At the same time, the US Federal Reserve’s (Fed’s) accommodative environment—put in place during the pandemic—impacted fixed income markets.

So far this year, market performance has been challenging across a broad range of asset classes. US equities, as measured by the S&P 500 Index, are down 14.04% through 6 May 2022. Growth-oriented stocks, as measured by the NASDAQ Composite, declined even more than the S&P 500. The broader bond markets, as measured by the Bloomberg U.S. Aggregate Bond Index, have also declined this year. Investment-grade and noninvestment-grade bonds within the aggregate index have also fallen, reflecting the broader rise in yields and some weakness in corporate credit spreads.

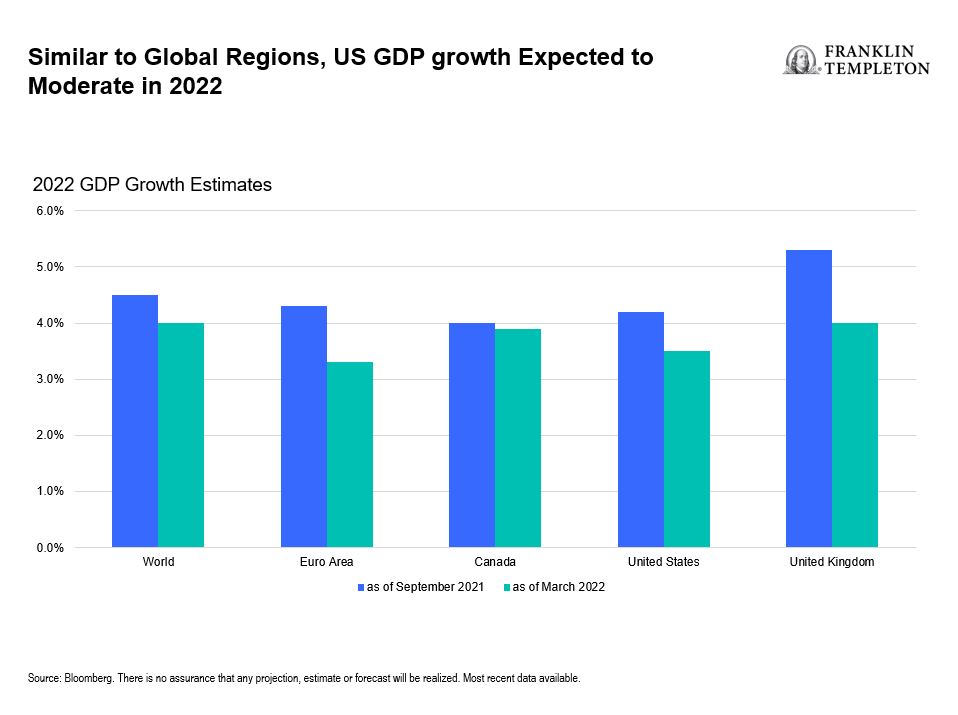

Entering 2022 Investors expected that US gross domestic product growth would decelerate, but we still believe growth is likely to be above long-term trends. In our opinion, it was inevitable that US year-over-year growth would slow following robust growth in 2021 as economies reopened. Also, the fading monetary and fiscal stimulus contributed to the US economy slowing. Economies worldwide are also moderating, with Canada doing better than other places due to the commodity-oriented nature of its economy.

Inflation Concerns Have Become Top Priority

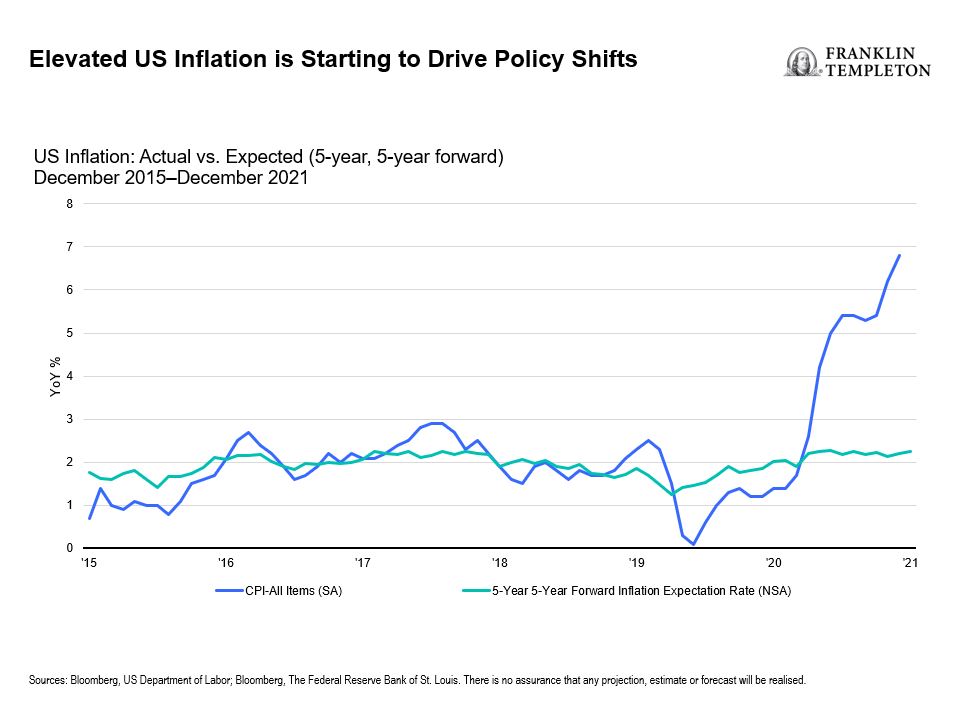

While economic activity in the United States has been normalising as it gets past the pandemic, a lot of inflationary pressures have been more pronounced and are rotating through different parts of the economy. This scenario is what is leading the Fed to raise the federal funds rate, and the market has baked in more frequent rate hikes for this year. These likely increases have rippled across the Treasury yield curve in general, which is what we believe is driving the challenging performance in fixed income markets. Thus, the backdrop remains highly uncertain in terms of the kind of tightening that is possible as the economy decelerates. In addition, there are other risks for investors—mainly geopolitical risks. These include of course the Russian-Ukraine war, which could further dampen economic activity in certain regions, particularly in the eurozone.

Consequently, rising inflation and its impact on the economy has become the primary focus. One of the bigger questions the market has right now is whether or not the Fed can successfully engineer a soft landing, or if a hard landing is more likely, given the pace of rate hikes and quantitative tightening starting up in June. With the Fed starting to make aggressive rate hikes and reducing its balance sheet, it is a dynamic time for the markets. Challenges are likely to stick around for quite some time. Thus, we believe that being nimble in finding opportunities will be critical.

Previous US rate hike cycles, specifically the last time the Fed raised rates in 2015–2018, played out over a long period of time as the economy generally slowed without elevating inflation. This time, it is radically different, with inflation at a very high level at the same time economic growth is decelerating. The United States has not experienced this type of inflation outlook in more than four decades, leading to newer challenges and uncertainties impacting current market performance.

Corporations Starting 2022 on a Positive Note

Historically, earnings expectations for companies tend to start the year on an optimistic note, and then decline over the course of the year. An exception was 2021, which started with a high degree of uncertainty around the level of earnings coming out of corporate America, but then surprised on the upside as companies managed supply challenges and other logistical issues.

As for the outlook for 2022, companies are generally performing well in terms of meeting first-quarter expectations. For the remainder of 2022, expectations are starting to come down as companies will likely vary in how they navigate the changing macroeconomic environment. Demand is still very strong, and challenges with logistics still exist; COVID-19 lockdowns are still occurring in China and may ripple through the United States and the world.

Meanwhile, the US labour market is nearing record low levels of unemployment, with elevated numbers of job openings. Employee sentiment is still high, and while tempered by market declines and higher inflation, household wealth and wages remain robust. The challenge for consumers is how to maintain purchasing power. In our analysis, the resilience of the US labour market—as well as how monetary policy transitions impact the economic outlook—could delay or prevent a US recession.

Franklin Templeton Key risks & Disclaimers:

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton’s U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What are the risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Franklin Templeton Investment Management Limited (FTIML). No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.