Jean Boivin, Head of the BlackRock Investment Institute, together with Wei Li, Global Chief Investment Strategist, Alex Brazier, Deputy Head and Vivek Paul, Head of Portfolio Research, all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Eyes on new regime: Policymakers are recognizing a new macro regime but are ignoring the trade-off between inflation and growth. A resulting recession is bad news for risk assets.

Market backdrop: Stocks fell last week after hawkish comments by Fed Chair Jerome Powell and data showing another month of jobs gains. We see the Fed hiking through 2022.

Week ahead: We expect the European Central Bank (ECB) to raise rates by 0.75% this week. We see it stopping well short of market projections in the face of recession.

We’ve argued for a while that we’re in a new macro regime. Central bankers at the recent Jackson Hole forum started to recognize this reality. But we think they’re not prioritizing economic implications over pressure to curb inflation. It seems they do not intend, for now, to manage the sharp trade-off between inflation and growth. That’s a big deal. We think getting inflation back to central bank targets means crushing demand with a recession. That’s bad news for risk assets in the near term.

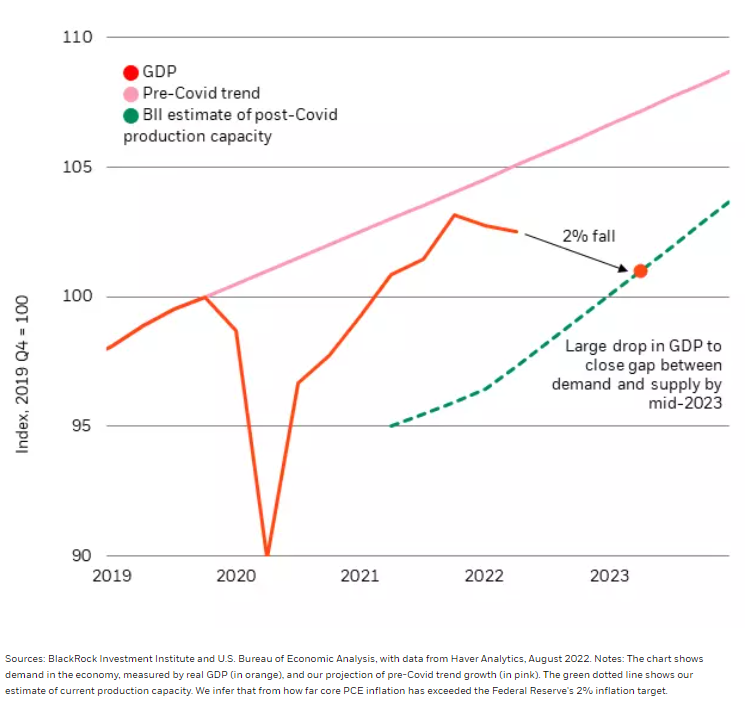

Mind the growth gap

U.S. GDP and production capacity, 2019-2024

The U.S. economy has already stalled. Now we see recession in the cards early next year. Powell made abundantly clear at Jackson Hole that the Fed has, for now, no intention of backing off its hiking cycle. The problem is that rate rises won’t solve the biggest issue: low production capacity (see green dotted line in chart). The only way the Fed can get inflation down quickly is by raising rates high enough to force demand (orange line) down by around 2% to what the economy can comfortably produce now. That’s well below the pre-Covid growth trend (pink line). But the Fed has yet to acknowledge the great cost to growth or the unusual nature of constraints in the labor market since the pandemic. We estimate 3 million more people would be unemployed if demand were to contract by 2%.

The Fed will be surprised by the growth damage caused by its tightening, in our view. When the Fed sees this pain, we think it will stop raising rates. It will be too late to avoid a contraction in economic activity by then, we think, but the decrease won’t be deep enough to bring PCE inflation down to the Fed’s target of 2%. Instead, we expect inflation to persist close to 3%.

The outlook for Europe

Europe is a different story; we’ve expected recession there for months given the energy crunch. By year-end, rate rises will push the euro area into a deeper recession. The European Central Bank (ECB) appears just as determined as the Fed to fight inflation by raising rates. At Jackson Hole, ECB executive board member Isabel Schnabel acknowledged a trade-off between taming inflation and maintaining growth. Yet she stressed a “robust control” approach to monetary policy, focused on getting inflation down at whatever cost. We think the ECB will hike 0.75% on Sept. 8. But like the Fed, the ECB is not grasping the full extent of the recession needed to crush inflation, in our view. We think the ECB will keep raising rates through the rest of the year but stop earlier and well short of market projections when faced with the gravity of the recession.

What this means for investing

The main conclusion: The new regime requires more frequent adjustments to portfolios. Time horizon is also key. In the short term, we’re underweight developed market (DM) equities on a worsening macro outlook. Central banks look set to overtighten policy and stall the economic restart. The recessions we predict are not priced into equities, we think. That’s why we aren’t buying the dip. Longer term, we’re modestly overweight DM equities. They have relative appeal over private growth assets – those have yet to reprice like their public counterparts – and fixed income, where we see higher yields dragging on expected returns. Sectors that we believe will benefit most from long-term trends like the net-zero transition, such as technology, are also particularly well represented in the DM equity universe.

Publicly traded credit is an overweight in our strategic portfolios for the first time in years as yields and spreads have materially repriced. That includes high yield. Tactically, we prefer to be up in quality in investment grade since we think it could better weather a slowdown that equites haven’t priced in yet. Lastly, we’re overweight global inflation-linked bonds, now and even more so further out. Why? We think markets are once again underappreciating the persistence of higher inflation. We’ve been arguing all year we’re in a new regime of heightened macro volatility driven by production constraints. In the near term, they are caused by Covid supply disruptions and labor shortages. In the long run, we see them pressured by structural forces such as a bumpy net-zero transition and a rewiring of global supply chains amid geopolitical tensions.

Market backdrop

Stocks ended lower in a volatile week after Powell’s hawkish Jackson Hole comments about the Fed’s “unconditional” objective to bring inflation back down to its 2% target. On Friday, U.S. jobs data showed another month of job gains alongside an increase in those searching for jobs. Given Powell’s tone, we see the Fed hiking through this year and think it will only stop tightening once it sees the damage to growth and jobs from higher rates.

The ECB will be the center of attention this week, and we expect it to raise rates by 0.75%. An ECB executive board member’s comments at Jackson Hole suggest the central bank is starting to acknowledge that reducing inflation to its 2% target will come at a sizable cost to jobs and growth. We’ll be assessing how much that’s reflected in the ECB’s updated forecasts. We see the ECB hiking rates through 2022 and then stopping amid an energy shock-triggered recession.

Week ahead

Sept. 5: China Caixin services PMI

Sept. 7: China trade data; U.S. trade data

Sept. 8: ECB monetary policy meeting

Sept. 9: China PPI and CPI data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 6th September, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.