Jean Boivin, Headof BlackRock Investment Institutetogether with Wei Li – Global Chief Investment Strategist,Alex Brazier – Deputy Head and Vivek Paul – Global Head of Portfolio Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Lessons learned: We think 2023 stressed the value of adapting to a new volatile macro regime, and leveraging investment insight and structural forces to find opportunities.

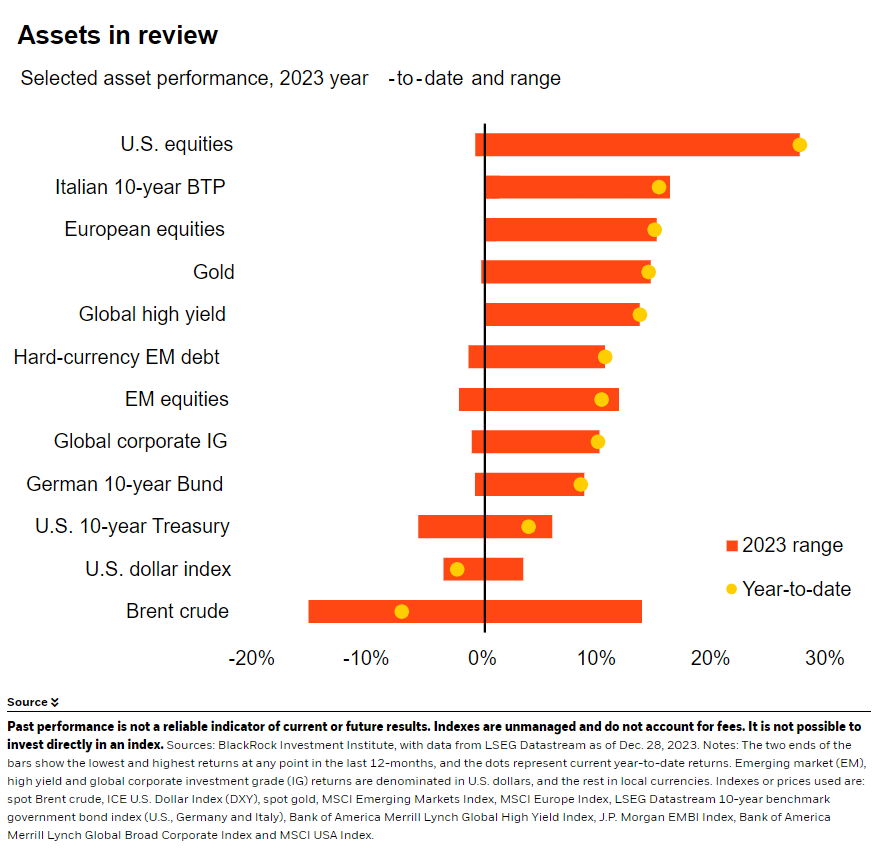

Market backdrop: U.S. stocks surged in 2023, a reversal from their 2022 underperformance. Flip-flopping market views about the policy path stoked volatility in long-term bonds.

Week ahead: December U.S. jobs data out this week should signal how much more the labor market needs to normalize. Slower jobs growth is a long-term supply constraint.

We take three lessons from 2023 to shape our investment approach in the new year. First, markets flipflopping between macro narratives does not reveal new information about where we will end up. This is not a typical business cycle and context is everything. Second, greater dispersion is creating opportunities. That requires skill and granularity. Third, artificial intelligence buzz has underpinned U.S. stock performance – and shows mega forces matter now, not just in the future.

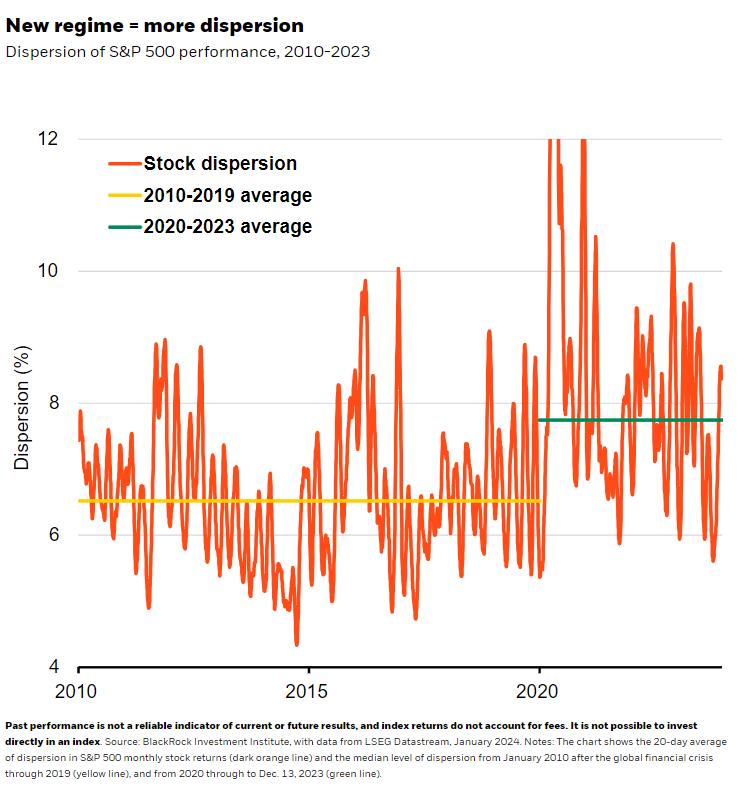

Looking back, 2023 largely saw a concentrated tech stock rally, with the Nasdaq up 55% from 2022. A market-wide rally since November also supported tech and led the equal-weighted S&P 500 to eke out a 12% return. Overall, we are seeing more dispersion in individual stock returns since 2020 (green bar in the chart). Macro uncertainty, geopolitics and structural shifts are driving volatility and dispersion. We think markets have stoked volatility, too, by viewing the new regime through the lens of a typical business cycle. Investors leaned into long-term bonds in early 2023 on hopes the Federal Reserve would cut policy rates by year end. It then became clear higher government spending and labor shortages are set to make inflation persistent and keep interest rates above pre-Covid norms. Ten-year Treasury yields surged to 16-year highs near 5% in October as markets priced in this outlook. They tumbled back below 4% by year end after the Fed blessed the pricing of rate cuts.

These volatile moves underscore the first lesson that was reinforced in 2023: The macro backdrop is much more uncertain today than during the Great Moderation period of stable growth and inflation. This is tough to navigate for markets, with them flipflopping between macro narratives through 2023. In the final quarter alone, both stocks and bonds surged on news of lower inflation – with the November PCE report confirming a goods-led slowdown – and dovish Fed projections. Small caps rallied on hopes for a soft economic landing. And markets have repeatedly priced in aggressive rate cuts just to walk them back. All this shows markets may extrapolate a lot from one piece of data or central bank comment. That’s taking a big bet on the macro outlook when the range of outcomes is wide, in our view. We don’t believe the prevalent market narrative tells us new information about where the macro will end up. Yet we are cognizant markets can run with a narrative for some time. This is why we turned tactically neutral on long-term U.S. Treasuries last October. We think long-term yields will resume their rise over time as investors demand more compensation amid persistent inflation and budget deficits.

Our second lesson

The greater macro risk means the dispersion of returns has increased. The result: a wide divergence in performance across equity sectors – and greater opportunities for investment expertise to shine, in our view. The correlation between bond and stock returns has flipped firmly into positive territory, meaning stocks and bonds fall or rise simultaneously. As a result, the old approach to portfolio construction that relied on bonds to offset equity sell-offs won’t work, in our view. Instead, we advocate breaking up broad asset allocation blocks and digging deeper. All this is why our second lesson is that granularity is more essential now. We look beyond the macro to seek above-benchmark returns, or alpha, by being dynamic and selective.

Our third lesson

One example of going beyond broad asset class exposures is to harness mega forces. The artificial intelligence (AI) mega force drove 2023 stock performance to an even larger extent than we had imagined. The importance of AI and other mega forces hammers home our third lesson: Structural forces matter now. Aging populations mean an ever-rising share of the population is past retirement age, resulting in worker shortages. That’s a key constraint fueling U.S. inflation now as a tight labor market keeps wage growth elevated. Others include the low-carbon transition and geopolitical fragmentation. The latter is evidenced by wars in Ukraine and Gaza and the intensifying structural competition between the U.S. and China.

Our bottom line

2023 emphasized the macro risks but also the opportunities on offer from structural shifts and getting granular in the new regime. Our 2024 Global Outlook outlines how we capture them.

Market backdrop

U.S. stocks surged roughly 25% last year, a near mirror image of their downtrodden 2022 performance. That was partly driven by excitement over AI lifting tech stocks and carrying the broader market. Meanwhile, the 10-year Treasury yield ended the year where it started: It climbed from lows of roughly 3.3% in April, to 16-year highs near 5% in October before falling below 3.9% at year end. We think some of the sharp swings in narratives – and markets – reflect the new regime of greater volatility.

We will be looking to the U.S. payrolls data for December out this week to gauge how much further the labor market has left to normalize in the new year after the pandemic. Structurally slower labor force growth is one of several long-term production constraints we think will prevent the U.S. and many other major economies from growing at their pre-pandemic pace without sparking renewed inflation.

Week Ahead

Jan. 3: U.S. ISM manufacturing PMI

Jan. 4: China Caixin services PMI

Jan. 5: U.S. payroll data; euro area inflation

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 2nd January, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

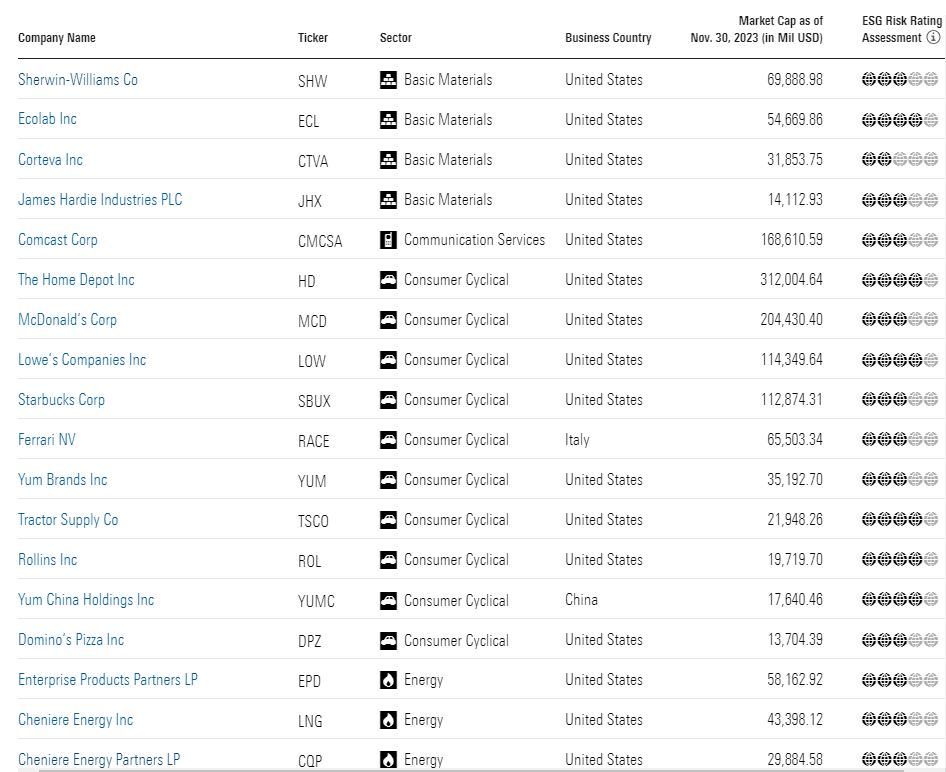

These companies stand out from the competition and can be good choices for long-term investing.

When you buy a stock, you own a piece of the underlying business. It’s important to understand the quality of the business you own, for the same reason you would test drive a new car before buying it.

The best companies tend to exceed your expectations. They find investment opportunities that you might not have thought about, or that you wouldn’t be able to pursue as an individual, increasing the intrinsic value of their business. Over time, these companies tend to be worth much more than they are today.

Long term, our analysts think having a stake in a high-quality company will put you in a far better position than chasing market movements or the brief boom of a low-quality business. With that in mind, here are a group of rock-solid companies that are truly positioned to stand the test of time.

What Makes a “Best Company”?

One of the keys to finding the best long-term investments is buying companies that can stay one step ahead of the competition. Legendary investor Warren Buffett originally coined the term “economic moat” to refer to a company’s ability to keep competitors at bay over time. Morningstar builds on this idea to rate companies based on their “moat,” or the strength and sustainability of their competitive edge.

We’ve compiled a list of the best companies our analysts cover that are available to U.S. investors. These companies have successfully carved out wide moats between them and their industry competitors, and we’re confident that they will produce returns that outweigh their costs for the next 20 years or more. In other words, these companies will reliably be able to produce returns for investors over a long period even as they invest in their growth. The strength of their competitive advantages is also either steady or increasing, which adds to our confidence in their long-term growth.

A company’s longevity and competitive advantage are inherently tied to sustainability, so our analysis takes environmental, social, and governance, or ESG, considerations into account. The best companies have business models that allow them to effectively navigate evolving ESG issues that could materially impact their business. Cutting corners or taking on too much risk may work in the short run, but these tactics won’t give a company enduring success.

The companies that make our list also have predictable cash flows (or predictable amounts of money going into and out of a company), so our analysts can more accurately estimate how much the businesses are worth. These companies also make smart decisions about how they manage and invest their money.

We aren’t advocating that you buy shares of every company on this list today. Even the greatest company can be a bad investment if you overpay. The share prices of many companies on this list overestimate their real value, so it may not be the right time to buy. Still, we believe these companies are essential for any stock investor’s watchlist.

We’ve grouped the companies on this list according to the overall sectors of the economy in which they compete.

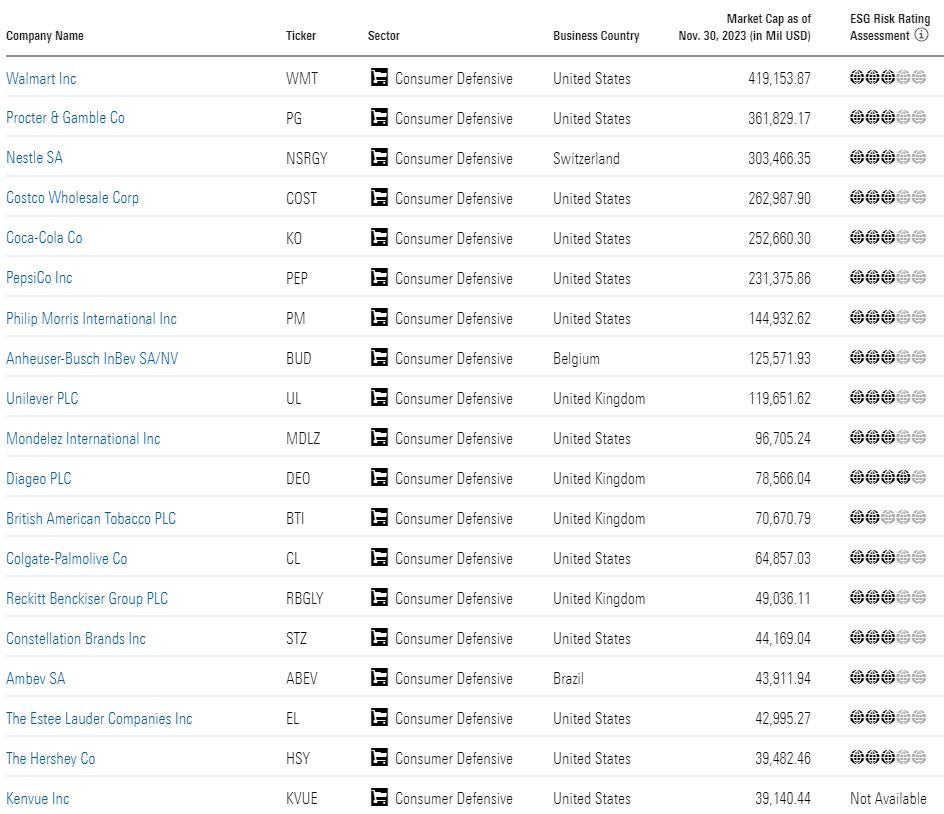

Consumer Defensive Companies

The consumer defensive sector isn’t what it sounds like. Think brands you find in your home—companies that manufacture household and personal products, food, and beverages. It also includes discount stores.

These companies provide services that consumers always need, so changes in the economy, like downturns, generally don’t have much impact on the sector. That’s where the “defensive” of consumer defensive comes in: The sector isn’t impacted by the ups and downs of the economy. Many of the companies below have strengthened their positions by developing a strong relationship with shoppers and offering either lower prices than their competitors or a strong brand identity that justifies higher pricing.

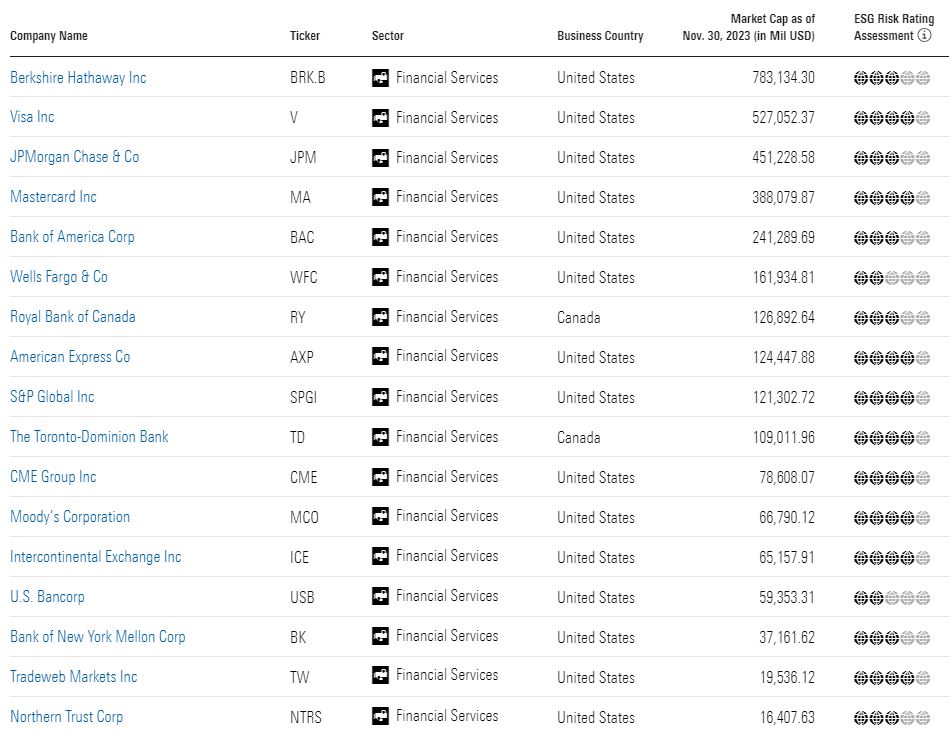

Financial Services Companies

The financial-services sector includes banks, asset managers, financial research and data companies, credit services, investment brokerage firms, stock exchanges, and insurance companies. Just as the services they supply differ, the companies below fend off competition in distinct ways. The most common characteristic among them is that their customers face relatively high hurdles when they want to switch service providers.

Many companies in this sector are economically sensitive with interest rates, the level of the stock market, and financial health of consumers and businesses affecting results.

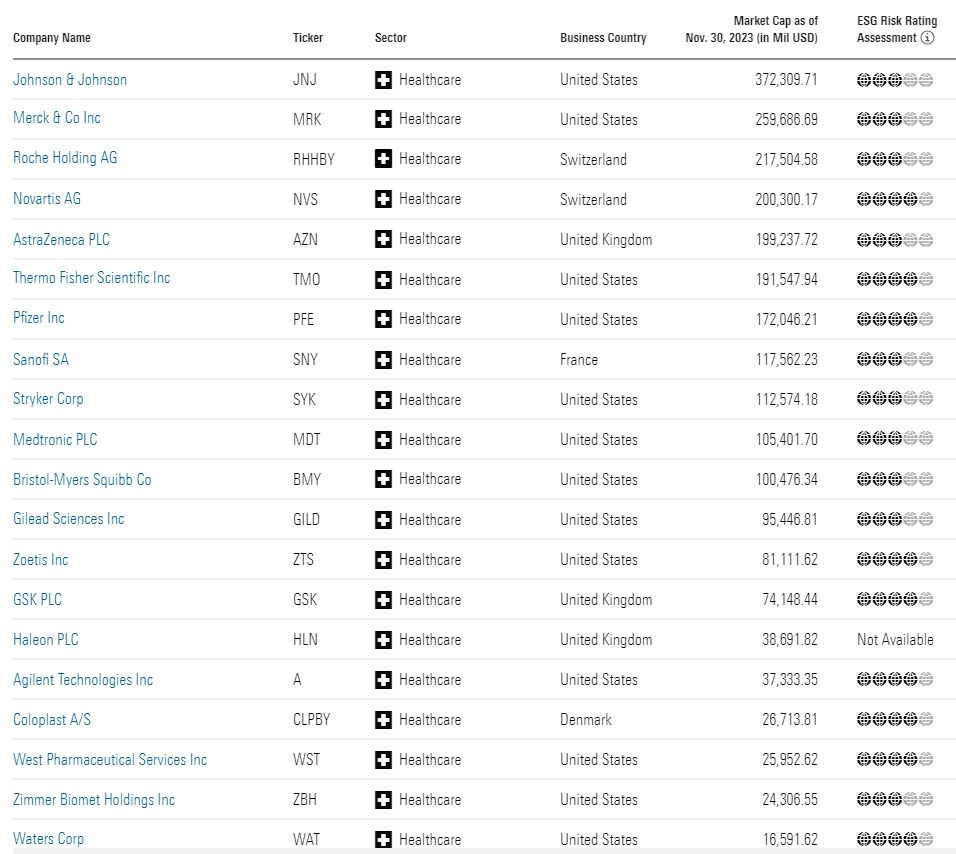

Healthcare Companies

Healthcare is another sector that generally holds steady no matter what is happening in the economy. The healthcare sector includes companies in biotechnology, diagnostics and research, drug manufacturing, and health information services.

Many of the high-quality healthcare companies that made our list are drug manufacturers whose patent protection keeps competitors at bay.

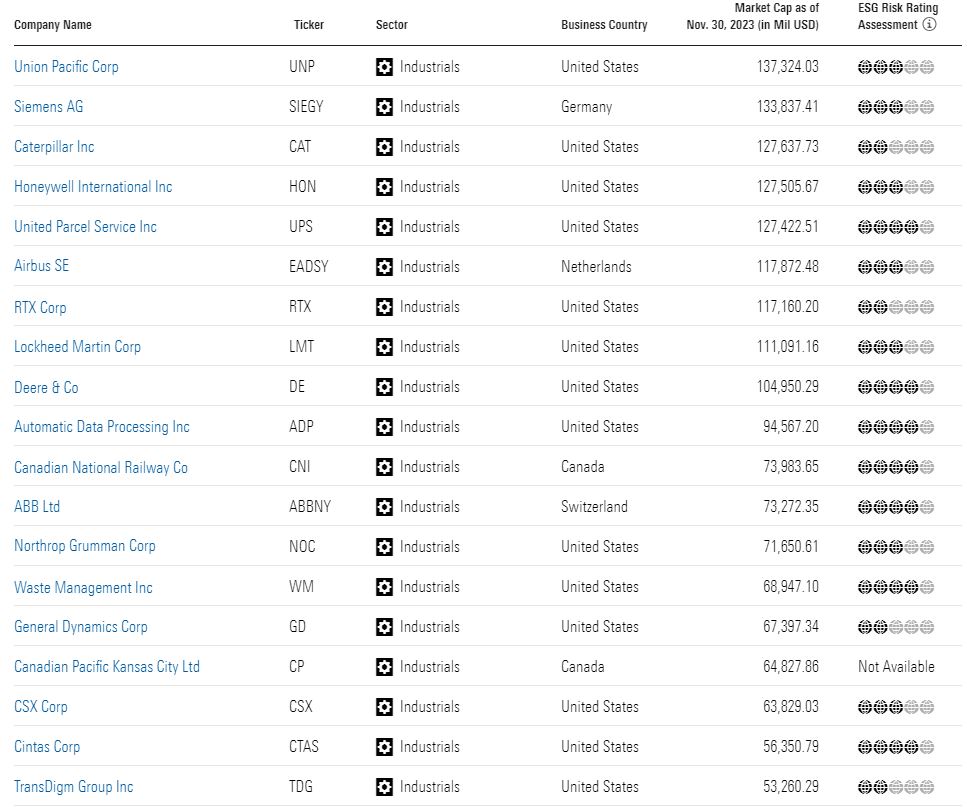

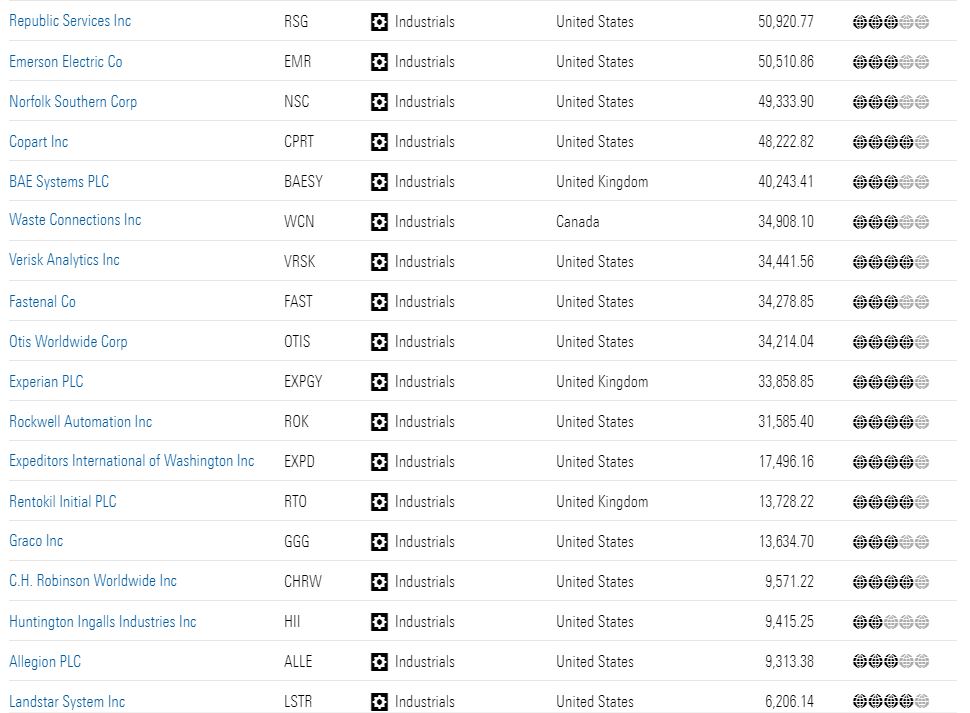

Industrial Companies

Planes, trains, and heavy machinery. Companies in the industrials sector support and transport all things industry. The sector includes companies that produce machinery, hand-held tools, and industrial products. It also includes aerospace and defense firms as well as transportation services. More companies from the industrials sector made our list than from any other group.

Many of these companies benefit from their incumbent position in their respective industries. It allows these businesses to develop brands and patents that give them their edge. Many further benefit from a cost advantage, operating in industries where infrastructure or regulation limitations make it expensive for new competitors to enter the market.

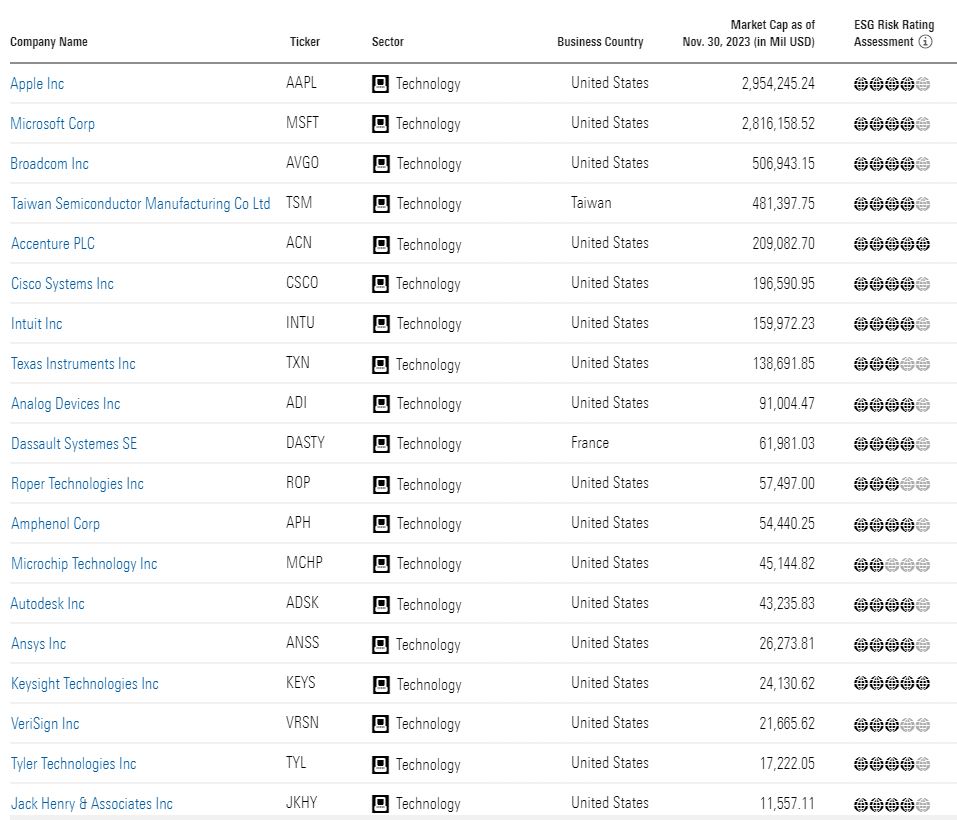

Technology Companies

Technology is an area that is infamously ripe for disruptors, but some companies have been able to carve out pockets of stability. Companies in the technology sector are engaged in the design, development, and support of computer operating systems and applications. This sector also includes companies that make computer equipment, data storage products, networking products, semiconductors, and components.

Many of the companies that made our list are software application developers that keep their position by providing services with high switching costs. Customers find it difficult to stop using their services because it’s hard to do, expensive, or risky to make the switch.

Other Sectors

The companies below represent various sectors: basic materials, communication services, consumer cyclical, energy, and utilities. Most of these sectors, except for utilities, ebb and flow with the overall economy, so predicting companies’ cash flows is more difficult.

Many of these companies also operate in highly competitive or evolving industries where it can be hard to create a sustainable competitive advantage.

Best Companies to Own 2024: Methodology

The companies on this list are covered by Morningstar Research Services’ equity analysts and have shares available to U.S. investors. This means that Morningstar equity analysts have calculated fair value estimates for the shares of the companies that trade on U.S. exchanges. As a result, most of the companies on this list are based in the United States.

Within that coverage list, the best companies meet the following criteria:

Wide Economic Moat. The Morningstar Economic Moat Rating summarizes the length of a company’s competitive advantages. An economic moat is really a structural feature allowing a firm to generate excess profits over a long period of time. If Morningstar Research Services believes that excess returns will persist for 20 years or more, that company earns a wide economic moat.

Standard or Exemplary Capital Allocation. The Stock Capital Allocation Rating is an assessment of the quality of management’s capital allocation, with particular emphasis on the firm’s balance sheet, investments, and shareholder distributions. Capital allocation is judged from an equity shareholder’s perspective, considering companies’ investment strategy and valuation, balance sheet management, and dividend and share buyback policies on a forward-looking basis. A company can receive an exemplary, standard, or poor capital allocation rating.

Low or Medium Fair Value Uncertainty. The Fair Value Uncertainty Rating represents the predictability of a company’s future cash flows and, therefore, the level of certainty in the fair value estimate of that company. The uncertainty rating for a company can be low, medium, high, very high, or extreme. It captures a range of likely potential intrinsic values for a company based on the characteristics of the business underlying the stock, including such things as operating and financial leverage, sales sensitivity to the economy, product concentration, and other factors. The more predictable cash flows, the smaller the range of potential intrinsic values, the lower the uncertainty.

Morningstar Disclaimers:

The opinions, information, data, and analyses presented herein do not constitute investment advice; are provided as of the date written; and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. The information presented herein will be deemed to be superseded by any subsequent versions of this document. Except as otherwise required by law, Morningstar, Inc or its subsidiaries shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. Reference to any specific security is not a recommendation to buy or sell that security. It is important to note that investments in securities involve risk, including as a result of market and general economic conditions, and will not always be profitable. Indexes are unmanaged and not available for direct investment.

This commentary may contain certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

The Report and its contents are not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Morningstar or its subsidiaries or affiliates to any registration or licensing requirements in such jurisdiction.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Morningstar, Inc. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. Any decision to invest should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

Morningstar are cautiously optimistic for both stocks and bonds as we enter 2024, even accounting for heightened risk.

In equities, we see opportunities in size, style, sector, and country exposures. Targeted exposure is well placed to beat broad market-weight exposure, according to our analysis. For bonds, we see broad appeal across different maturity profiles. Government bonds are our preferred exposure. Corporate bonds are priced for a slowdown, but not a recession, so they could carry heightened risk. The U.S. dollar looks expensive versus other major currencies, so international currency positioning (and possibly hedging) may be a worthwhile addition to your portfolio toolkit.

Equity Opportunities

Among the basket of undervalued and unloved assets, smaller-capitalization value stocks stand out.

Cyclical sectors like financials (namely banks), leap out as attractive. Among economically sensitive sectors, communication services remain appealing. Among defensive sectors, healthcare and utilities could offer a ballast with upside potential.

Global contrarian plays include the United Kingdom, emerging markets equities, and, specifically, Chinese technology. The volatility could be worth it, but sizing is important.

Second-derivative artificial intelligence plays, primarily in the U.S. market, could offer an earnings tailwind.

The Broad Equity Landscape Entering 2024

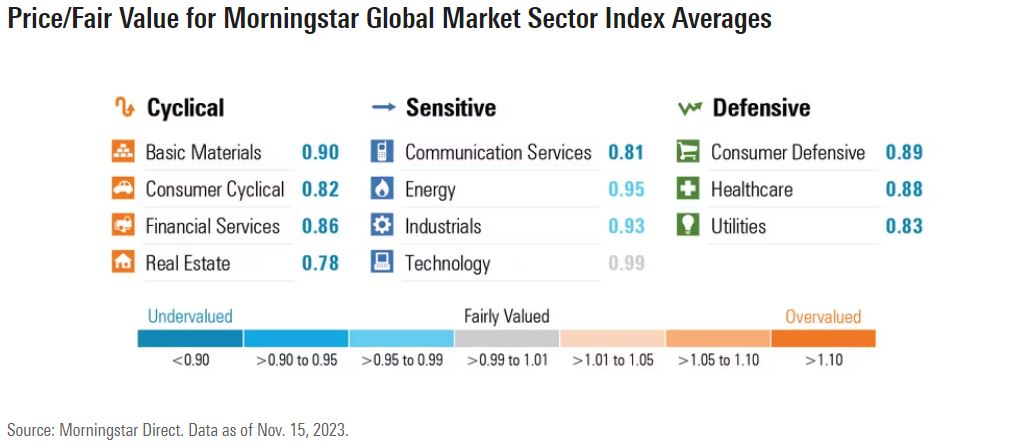

Equities look fairly well positioned as we start 2024, despite facing a wall of worry. Stocks are reasonably valued overall, with all major countries better placed than a few years ago from a valuation standpoint.

Overall, we see U.S. equities as playing a role for investors, although the concentrated rise in the so-called “Magnificent Seven″ has created opportunities to add selected value—which looks especially interesting in smaller, value-oriented companies. In other developed markets, we see attractive valuations with higher-than-usual return prospects on our analysis, especially in pockets of Europe (for example, U.K. and European energy stocks). While emerging markets are undoubtedly risky, we can see strong return prospects in most scenarios, although position sizing remains important.

Naturally, reward for risk is the key distinction to make, with some developing risks that must be accounted for in equity allocations. One longer-term risk is the lack of earnings growth. This is a challenge because investors have been driving prices higher relative to earnings—a dynamic known as multiple expansion. One potential reason for the expansion of multiples this year was a belief that central banks would quickly and aggressively pivot to cut rates. This is no longer the consensus base case.

Here are some of the key risks we’re watching:

Moderate Valuations

Valuation expansion has largely been in AI stocks. Second-derivative AI stocks have not had the same rally.

The U.S. market contains some expensive sectors and concentration risks.

Select opportunities exist in global equities.

Softening Economy

High rates can weaken consumer demand, particularly if they persist.

A weaker consumer can impact corporate revenue and ultimately the labor market.

Weaker European countries may trough sooner than the U.S. market.

Weakening Fundamentals

In the United States, overall corporate leverage is manageable, but debt costs are increasing.

Corporate profitability is high, but vulnerable on the margin.

Capital-intensive sectors remain more exposed to a protracted move higher in debt costs.

External Shocks

Geopolitical risk is high (Ukraine, Israel, and China).

An oil market shock could hurt the global economy.

Commercial real estate remains a risk but appears to be a localized problem.

Suddenly higher long-term yields could have unintended effects.

While stocks have certainly not tumbled off a cliff, investors continue to feel nervy, with consumer sentiment scores still well below normal levels. At a deeper level, valuation spreads—the disparity in valuation levels between sectors—is where we see opportunity.

Equity Opportunity 1: Select Sectors—Including Financials, Utilities, and Healthcare

With U.S. index returns having been driven predominantly by large-cap growth companies that dominate index weightings—aka the “Magnificent Seven″—we’re finding valuation opportunities elsewhere.

Financial services, squarely a cyclical value-leaning sector, leaps out as inexpensive with low expectations. Rising rates and the 2023 U.S. banking crisis led the sector to underperform. We believe much of the risk here has been discounted and that U.S. banks, in particular, are worth a look.

Looking for undervalued assets that can help with portfolio robustness, we see defensive sectors—including healthcare and utilities—as areas of interest. They are not necessarily the cheapest sectors but can play a strong role in portfolio risk management. Among the more economically sensitive sectors, our preference remains for communication services, despite strong returns for the year to date, as it still represents solid value and reasonable risk/reward, in our view.

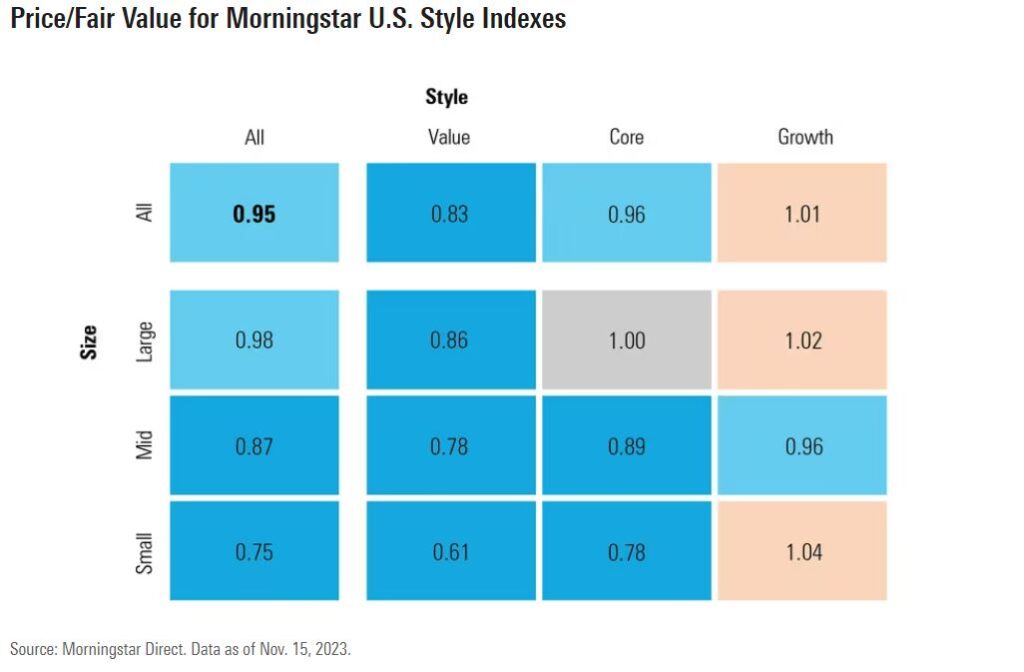

Equity Opportunity 2: Small-Cap Value Stocks

Looking at the Morningstar Style Box across the U.S. and Europe, we can see that the biggest valuation opportunity exists in the bottom left corner—small-value stocks.

In our latest U.S. Stock Market Outlook, this represents a large discount to fair value, which is considerably better than the large-growth counterparts that have dominated 2023 leaderboards. You can see a similar discount in our European Equity Market Outlook.

We note that small-cap stocks are hard to place in a single bucket, in large part because so many disparate industry groups—from biotech to banks—are part of this asset class. Plus, small companies generally display greater sensitivity to the broad economic environment, given the preponderance of money-losing and highly leveraged companies in the small-cap indexes.

Therefore, while small-cap stocks seem substantially cheaper than their large-cap counterparts, careful asset selection is needed, and we think it’s important to focus on quality.

Equity Opportunity 3: International Exposures—Including the U.K., European Energy, Emerging Markets, and China Tech

While U.S. equity returns have been dominant over recent years, we think there is a significant opportunity for investors looking outside the U.S. Our work suggests that the U.K., with a significant amount of the index consisting of a well-diversified group of global companies, including both cyclical and defensive components, represents good value. Plus, cyclical industries such as European energy companies, which are displaying significantly improved capital allocation amid robust energy markets, look comparatively cheap. The broad opportunity in emerging markets has grown more significant during 2023, as those stocks have lagged their developed-markets peers.

Much of the performance drag can be attributed to Chinese stocks as investors weighed looming geopolitical and secular growth concerns. The aggregate sentiment toward emerging markets remains bearish in absolute (compared with its own history) and relative terms (compared with developed markets).

Despite the risks—or maybe because of them—China itself has become a very interesting opportunity. Chinese equities carry particularly low expectations. However, over the long term, consumer-facing Chinese technology equities trade at a substantial discount to normalized earnings and are anticipated to generate excess returns against broad emerging markets.

Equity Opportunity 4: Second-Derivative AI Plays

AI-focused stocks have topped the leaderboard in 2023, with significant valuation risks embedded, in our analysis. However, second-derivative plays, including those that can improve margins by using AI capabilities in their products, offer much better valuations with earnings upside.

This could offer a way to access the emerging AI theme, with generative AI allowing companies to generate marketing content, write code, and improve efficiency, among other things. No doubt this will create winners that can harness the benefits of AI with the ability to massively scale businesses and losers that cannot.

Fixed-Income Opportunities

Areas with positive real yields. Broad opportunities exist, especially in developed markets. However, niche opportunities also appeal, including inflation-linked bonds, U.S. agency mortgage-backed securities, and emerging-markets debt.

Government bonds over corporate bonds. In particular, U.S. Treasuries look well positioned, with the balance of probable outcomes for yields leaning toward falls.

Short-duration bonds are attractive for cautious portfolios, adding healthy income with appropriately lower duration risk.

The Broad Fixed-Income Landscape Entering 2024

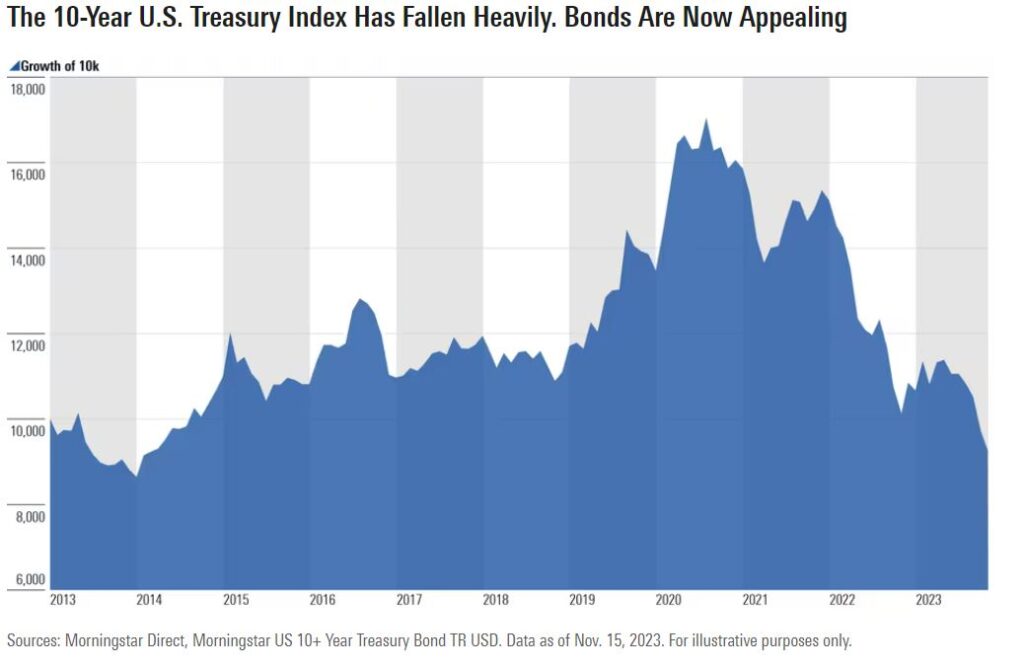

The bond market has not provided the defensive features over the past two years that investors grew to love it for in the four decades before July 2021. It has been one of the worst periods on record for developed-markets bonds in 2022 and into 2023.

This is especially true for long-dated bonds.

The potential long-term regime for inflation and rates has affected these bonds with equitylike drawdowns. We now see this as a positive in a forward-looking context. The material increase in bond yields has improved their attractiveness versus other assets and for portfolio risk management more generally.

This applies to the U.S., U.K., and Australia, where yields now cover inflation in many instances, offering positive “real” yields. European yields are also rising strongly but—from a very low base—exhibit less attractive absolute yields to date.

Going slightly deeper, the ability to add income to portfolios while mitigating default risk looks attractive to us currently. Duration risk again looks attractive in many scenarios, but it requires prudent management. We are cognizant of the potentially sizable drawdown risk from longer-duration assets. Adding materially to duration might make sense at some point, but any changes should be measured and deliberate, given the fast-changing response from central banks and the threat of stickier inflation. One key consideration in a portfolio context is reinvestment risk, with short-dated bonds offering strong yields but which could be left behind if rates get cut.

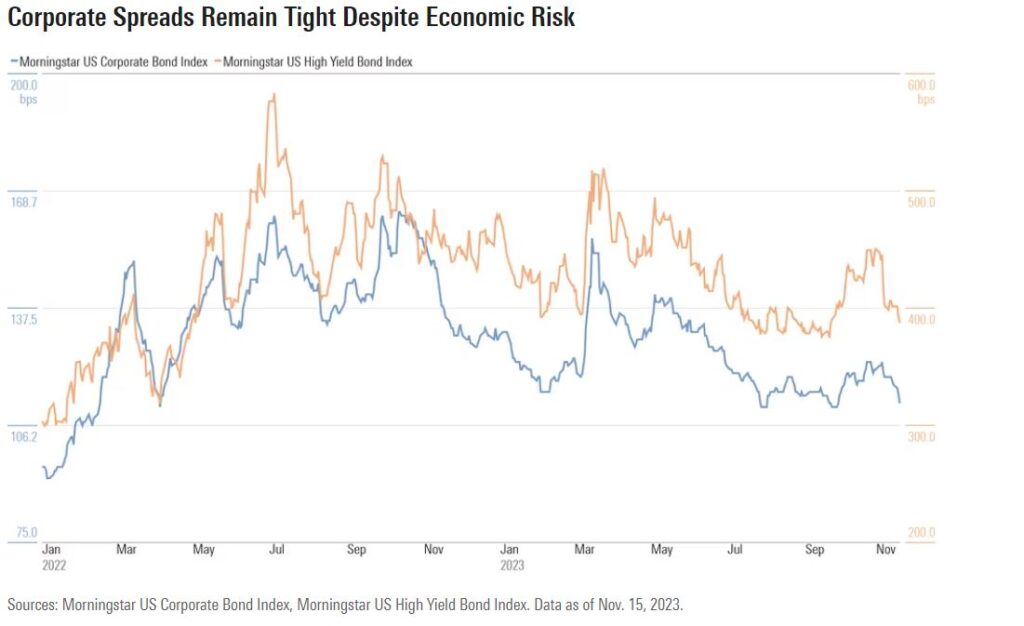

Corporate bonds, whether investment grade or high yield, offer higher yields than government bonds (given greater credit risk), although the “spread” between the two remains tighter than we might prefer, given the environment. They have a place as a middle ground—providing some extra yield versus government bonds and a duration profile that can help in portfolio construction.

Other bonds, including emerging-markets debt, retain appeal. However, we’ve softened our conviction in this space as developed peers now offer more appealing prospects. Our view remains that many emerging-markets sovereigns, though with notable exceptions, have improved their fundamental strength compared with history. This includes improved current account balances, enhanced reserves, movement to orthodox monetary policy, and a buildout of a local investor base allowing for a shift to local-currency funding.

In all cases, the key risk for fixed income is that interest rates fail to sufficiently slow economic growth and inflation. For this reason, inflation-linked bonds have appeal as a reasonably cheap form of insurance.

Bonds Opportunity 1: Focus on Positive Real Yields

A slew of opportunities now exist with positive real yields. This is a fantastic pond to fish in, with several opportunities apparent:

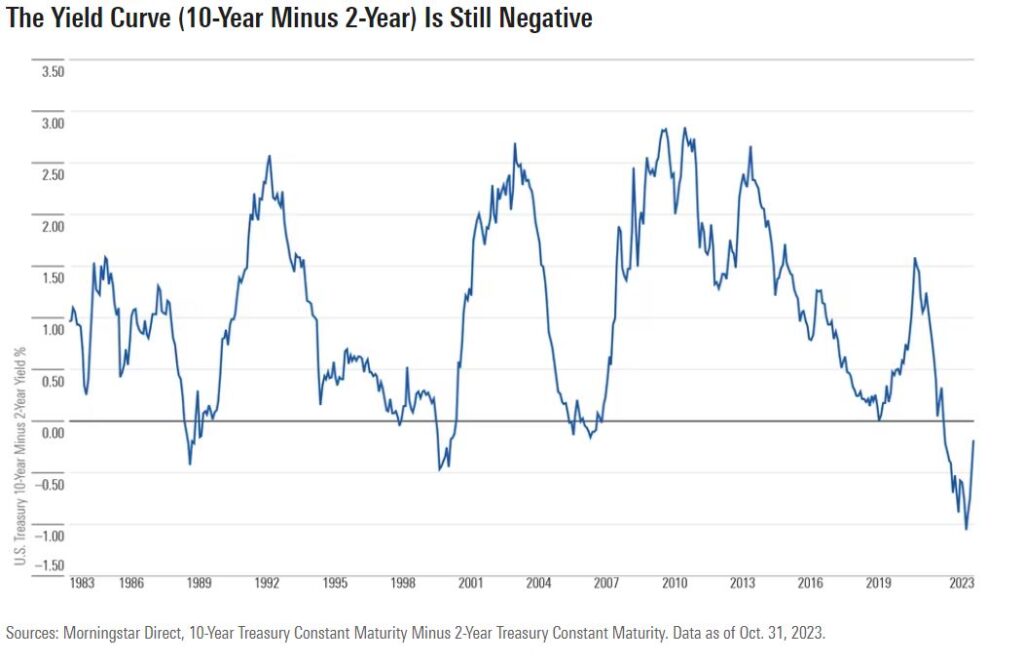

Developed-markets bonds, excluding Japan.Wehave seen significant moves across the yield curve. Higher yields make these bonds more attractive, especially shorter-dated bonds where an inverted yield curve exists. The defensive attributes are appealing. On the contrary, Japan is an area to be avoided, in our view, with negative real yields persisting.

U.S. agency mortgage-backed securities.We note solid fundamentals. Given the sharp rally in mortgage rates and significant duration extension, the attractiveness of this asset class looks appealing to us. The idea of slowing economic activity could support higher-rated assets, such as agency MBS, with little default risk. That said, further spread-widening may take place before moving in investors’ favor should the economic environment turn weaker.

Emerging-markets debt still offers attractive yields and prospective currency returns, even accounting for risk. This applies across local- and hard-currency offerings, although sizing is important.

Inflation-linked bonds continue to warrant some attention as they have repriced more attractively. Low inflation expectations make this a cheap form of insurance, with positive real yields now available.

Bonds Opportunity 2: Short-Dated Bonds for Cautious Portfolios

The yield on short-dated bonds still exceeds long-dated bonds. This is coming from an unusual base in a historical context, creating the so-called “inverted yield curve” we still have today.

To take advantage, it can be tempting to favor short-dated bonds. This is certainly sensible in an absolute sense, although the time frame matters. For investors who are cautious and/or have a short time horizon, short-dated bonds certainly appeal. We do note this brings reinvestment risk, which is notable if interest rates go down as expected. It may not be possible to lock in today’s long-term rates forever.

In practice, we think short-dated bonds are attractive given the inverted yield curve, so we have a great starting point—with a big gap between the current yield and our fair value yield at the short end of the curve. But for investors with longer horizons, we see merit in exposure across the maturity profile.

Bonds Opportunity 3: Overweight Government Bonds Versus Corporate Bonds

In this environment, we don’t need to stretch for yield. Government bonds in the developed world currently look as attractive to us as we’ve seen in at least a decade. This view holds across all durations.

At the same time, corporate bonds also look attractive, but the “spread” between them is on the tight side.

This is best expressed by watching credit spreads, which would usually increase if economic vulnerabilities rise. Yet, we haven’t seen spreads budge, so corporate bonds (both investment grade and high yield) lose relative appeal given the risk of economic deterioration.

For this reason, our analysis leads us to favor government bonds—particularly U.S. Treasuries—on a risk-adjusted basis. Withstanding another serious inflation run, the skew of upside to downside looks favorable to us. Of note, we do see appeal in short-term corporate bonds, where we can achieve positive real yields.

Another Idea for Your Toolkit: Currency Management

While stocks and bonds look broadly attractive to us, we do seek opportunities from across the entire investment universe. As such, we offer yet another idea for your toolkit, before summarizing the collection of our favored investment ideas: currency management.

The U.S. dollar looks expensive, although it still acts as a flight to safety in turbulence, so prudent international currency positioning (and possibly hedging) is an attractive dimension of portfolio management.

While currencies are notoriously volatile, we tend to think of currency positioning via the lens of portfolio robustness (focusing on those currencies with defensive characteristics where sensible), but also as a potential source of upside at extremes. Looking ahead, we continue to see merit in currencies outside the U.S. dollar. The yen has the potential to provide diversification qualities and potentially help preserve capital in times of extreme economic and market stress, as well as provide potential upside.

A Positive Take on 2024: Summary of Portfolio Opportunities

Taken together, the list below culminates our best ideas. By balancing these convictions into a broader diversified portfolio, we foresee a positive outlook for 2024 and beyond.

International-equity opportunities

The healthcare, financial-services (namely banks), and utilities sectors

Small-cap and value stocks

Second-derivative AI stocks

Positive real yields in fixed income

Treasuries over corporates

Diversified currency outside U.S. dollar

Morningstar Disclaimers:

The opinions, information, data, and analyses presented herein do not constitute investment advice; are provided as of the date written; and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. The information presented herein will be deemed to be superseded by any subsequent versions of this document. Except as otherwise required by law, Morningstar, Inc or its subsidiaries shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. Reference to any specific security is not a recommendation to buy or sell that security. It is important to note that investments in securities involve risk, including as a result of market and general economic conditions, and will not always be profitable. Indexes are unmanaged and not available for direct investment.

This commentary may contain certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

The Report and its contents are not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Morningstar or its subsidiaries or affiliates to any registration or licensing requirements in such jurisdiction.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Morningstar, Inc. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. Any decision to invest should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

You are leaving medirect.com.mt

Please be aware that the external site policies, or those of another MeDirect website, may differ from this website’s terms and conditions and privacy policy. The next website will open in a new browser window or tab.

Note: MeDirect is not responsible for any content on third party sites, nor does a link suggest endorsement of those sites and/or their content.

We strive to ensure a streamlined account opening process, via a structured and clear set of requirements and personalised assistance during the initial communication stages. If you are interested in opening a corporate account with MeDirect, please complete an Account Opening Information Questionnaire and send it to corporate@medirect.com.mt.

For a comprehensive list of documentation required to open a corporate account please contact us by email at corporate@medirect.com.mt or by phone on (+356) 2557 4444.