Jean Boivin, Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Alex Brazier – Deputy Head and Tara Iyer – Chief U.S. Macro Strategist all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

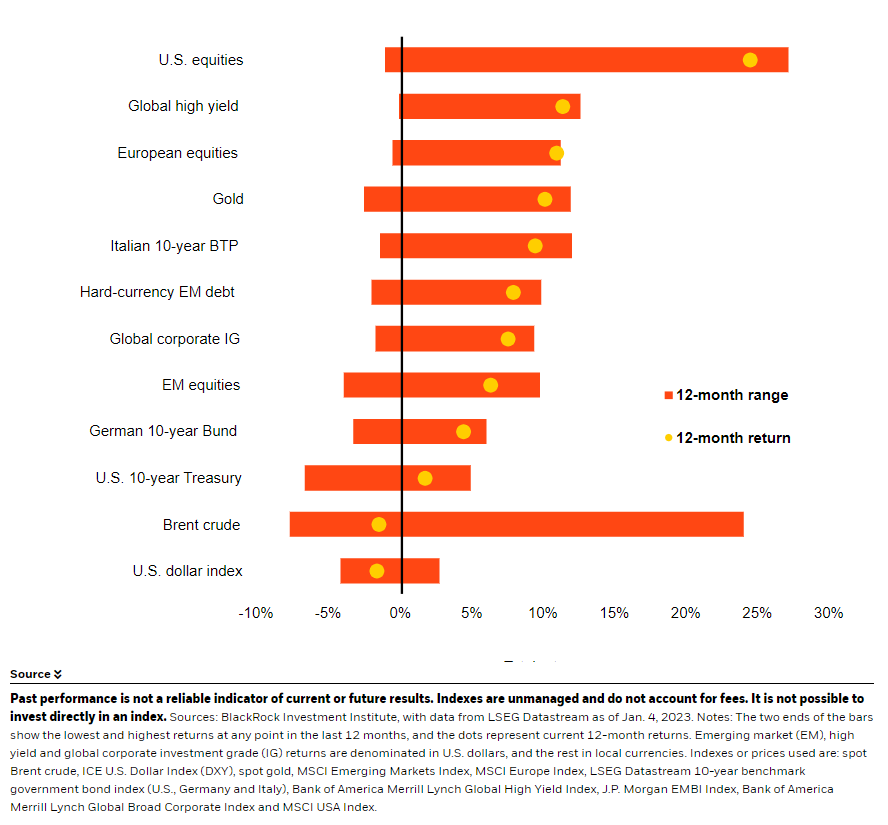

Year-end rally: Risk assets surged to end 2023 as the Federal Reserve blessed market hopes for rate cuts. That momentum could persist for some time as inflation cools.

Market backdrop: Stocks slid and bond yields rose last week. Data pointing to sticky U.S. wages showed why we think market optimism on inflation may eventually be let down.

Week ahead: The U.S. CPI this week will likely show falling goods prices leading inflation lower in 2024. We see supply constraints putting inflation on a rollercoaster.

Risk assets ended 2023 on an upbeat note as the Fed appeared to make a big bet on inflation coming down and growth only gradually slowing. Markets interpreted the Fed’s messaging as a green light for aggressive policy easing. The end-2023 rally could keep going well into 2024 as inflation cools further. Yet the jittery start to 2024 for stocks and bonds suggests investors may be nervous about the macro outlook. We stay nimble and think macro risks need to be deliberately managed.

The U.S. 10-year Treasury yield closed the year roughly where it started – at about 3.8% – masking a major round trip between 3.3% and 5%. U.S. stocks ended 2023 just below their all-time high largely thanks to the Fed unexpectedly making a big bet for the market by seeming to endorse expectations for aggressive rate cuts at its last policy meeting of the year. That once again highlighted how hopes and disappointments about the Fed drove market flip-flops throughout 2023. The final rally was no different, in our view. It has left equity markets priced for a near-perfect outcome: a soft landing, where inflation falls and central banks sharply cut rates. Market pricing implies they would come to the rescue with even bigger rate cuts if growth risks emerge. That’s why we think expected bond volatility remains high (yellow line in chart) relative to subdued expected volatility in stocks (orange line).

Markets interpreted the Fed’s communications around a potential peak in U.S. interest rates as opening the door to sharp rate cuts as inflation falls. We expect inflation to ease close to 2% in 2024 as consumer spending normalizes from the pandemic and goods prices fall. So beyond the early January jitters, the risk rally could extend – until the risk of inflation resurging comes into view later this year, as we expect. Markets pricing in a perfect outcome is a big macro bet, in our view. A soft economic landing is possible, but the range of potential outcomes is wide in the new regime of greater macro and market volatility. That’s why we’re ready to be nimble and selective on our six-to-12-month tactical horizon.

An inflation rollercoaster

Case in point: Falling U.S. goods prices are dragging down inflation as pandemic-driven swings in spending unwind. Yet a tight labor market is driving stubbornly high wage growth, as seen in the December jobs data. We think that means inflation is set to rollercoaster back up near 3% in 2025 as the goods price drag fades. We see geopolitical fragmentation bolstering inflationary pressures in coming years, too. That’s why we think the Fed may not be able to deliver the rate cuts markets expect, even with growth moderating as consumers exhaust their pandemic savings and government spending on defense and student loan forgiveness tapers off. The big question for risk assets: when they might start to reflect this outlook in 2024.

In fixed income markets, we see more volatility ahead partly as inflation’s persistence becomes clearer. Plus, we see markets grappling with where neutral rates – the interest rate that neither stimulates nor restricts economic activity – are settling after the pandemic. We think neutral rates are higher in both the U.S. and Europe, partly due to looser fiscal policy and the investment demands tied to the low-carbon transition. We also think investors could demand more compensation for the risk of owning long-term bonds given rising public debt and a more uncertain inflation outlook.

Our bottom line

We get granular to navigate macro uncertainty, favoring Japan, tech and industrials in stocks. We also went tactically neutral long-term Treasuries in October and we keep our overweight to short-term Treasuries. Yields may swing in either direction as markets keep reassessing the outlook for policy rates.

Market backdrop

The S&P 500 fell about 2% last week after the 24% surge last year, while U.S. 10-year yields climbed back to around 4% and rose more than 25 basis points from the December low. The Fed’s December meeting minutes highlighted the easing of financial conditions, adding to the risk asset jitters to start the year. The end-2023 market momentum could persist. But the December U.S. payrolls report confirmed ongoing wage pressures may ultimately disappoint the optimism on inflation.

We’re watching U.S. inflation data out this week to see if falling goods inflation will pull inflation further down in 2024 as pandemic mismatches unwind. Yet we think tight labor markets and slowing job growth will keep inflation on a rollercoaster beyond 2024. China macro data out this week will also help gauge how subdued activity remains. China’s economy faces two key challenges: sluggish consumer spending and weak demand for its exports.

Assets in review

Week Ahead

Jan. 9: Japan CPI

Jan. 11: U.S. CPI

Jan. 12: China CPI and trade data; UK GDP

Jan. 10-17: China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 8th January, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.