MeDirect has continued its blood donation campaign with a group of employees visiting the National Blood Transfusion Centre in Gwardamangia for the third time in less than 12 months. This initiative will continue in the months ahead with further blood donations being organised by MeDirect on a quarterly basis.

Blood donations from the public are vital in helping all of Malta’s public hospitals to deliver essential services. These include facilitating major surgeries and the treatment of cancer patients. All healthy persons aged between 17 and 68 can donate blood with males able to donate every 3 months and females every 4 months until one year after the menopause when they can also start donating every 3 months.

Emma Camilleri, Chief People Officer at MeDirect Malta, said, “Every drop of blood donated has the potential to save lives. This makes blood donations a powerful symbol of compassion and solidarity. We are incredibly grateful to our MeDirect colleagues who continue to offer their unwavering support to this campaign.”

More information on donating blood can be found here.

Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Vivek Paul – Global Head of Portfolio Research, Devan Nathwani – Portfolio Strategist and Natalie Gill – Portfolio Strategist all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

More active long term: We think market optimism can persist for now but stay nimble. We get more active in our long-term portfolios given a greater dispersion of returns.

Market backdrop: U.S. stocks steadied after a brief dip on stronger-than-expected inflation data last week. We think that shows one data release won’t spoil upbeat risk appetite.

Week ahead: Global manufacturing and services activity is in focus this week. The data may offer an early gauge of Q1 GDP growth as central banks hold policy rates steady.

U.S. stocks recovered after a hit from strong inflation data last week, highlighting one data point won’t disrupt buoyant risk appetite. We’re tactically overweight U.S. stocks as we think market optimism can persist for now. Yet we are strategically active – or ready to pivot our views as we expect resurgent inflation coming into view to spoil sentiment. In the long term, we see a greater role for active strategies that can produce above-benchmark returns due to richer asset valuations broadly.

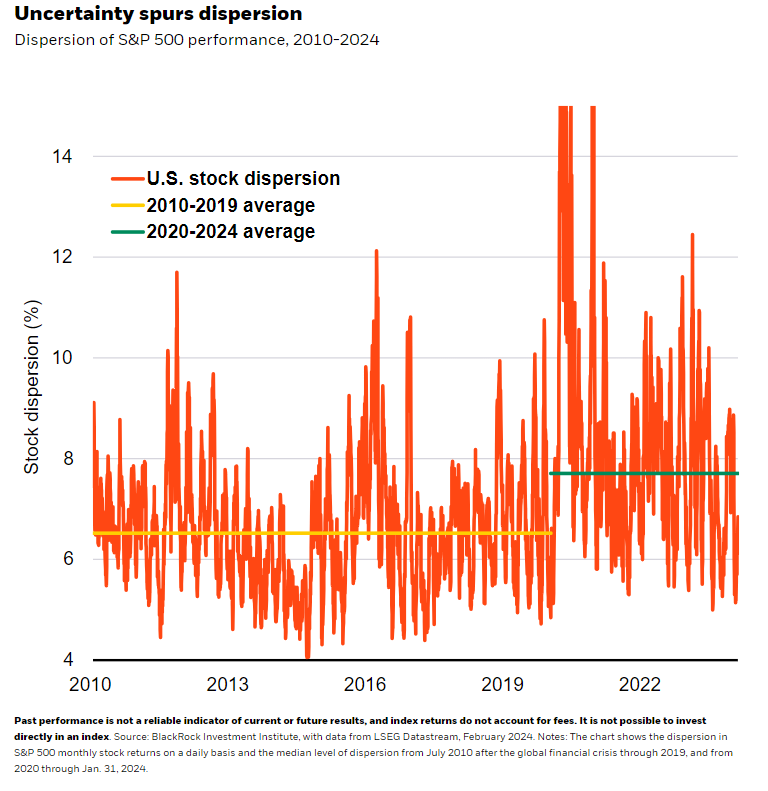

We believe there is less consensus and more uncertainty about key macro variables, like inflation, than in the past. Elevated uncertainty is reflected in the heightened dispersion of returns in the new regime, we find. Monthly returns of individual S&P 500 stocks (orange line in the chart) have deviated more from their average since 2020 (green line) than in the prior decade (yellow line). We opted to be selective in U.S. stocks as a result last year, leaning into the artificial intelligence (AI) theme and away from the broad market. Last month, we turned overall overweight U.S. stocks on a six- to 12-month tactical horizon, while still preferring tech. That’s because we think positive market sentiment can persist and broaden out for now as the Federal Reserve readies to cut interest rates and inflation falls nears its 2% target this year.

Yet we are nimble in reassessing our views given our expectation inflation will resurge in 2025. We think mega forces – big structural shifts like geopolitical fragmentation, demographic divergence and the low-carbon transition – are set to make inflation more volatile and settle higher than before the pandemic. On a strategic horizon of five years and more, our stance on developed market (DM) stocks is less positive than our tactical view and we stay neutral. Persistent inflation means real returns, or those exceeding inflation, will be lower over a strategic horizon. Long-term valuations for some asset classes look too high when baking in this outlook and our expectation for interest rates to settle higher than before the pandemic.

Why we get dynamic

That return outlook means that the traditional portfolio approach of static asset allocations won’t work as well as in recent decades, in our view. We stay dynamic in our strategic views as one part of the solution. We trim our overweight to inflation-linked DM bonds as real yields have slid. We up investment grade credit to neutral on a preference for Europe, where credit risk seems better rewarded. In addition to being more dynamic, we think active strategies will play a greater role in strategic portfolios. Our work finds that the difference in our estimate of active returns between the top and bottom 25% of managers is near its widest since 2011. Skill and acting more frequently on good insights can be better rewarded now, in our view.

Top managers may have more potential for active returns in private markets. Dispersion across them has risen in the new regime and tops public markets, based on the limited data available from NCREIF. We prefer income private markets over growth as a shifting U.S. corporate funding landscape likely boosts demand for private credit – part of the future of finance mega force. We see infrastructure equity as a bright spot within growth private markets as it cuts across all mega forces. Private markets are complex, with high risk and volatility, and aren’t suitable for all investors.

Our bottom line

We’re being strategically active in our portfolios. We’re overweight U.S. stocks tactically as we think positive risk appetite can persist for now, yet we stay nimble. We take a more active approach in the long run as structural shifts play out. Professional investors can visit our Capital market assumptions website for more details on our strategic return expectations.

Market backdrop

U.S. stocks steadied last week, recovering from a brief dip after U.S. CPI inflation data for January was stronger than expected. U.S. 10-year Treasury yields jumped as markets priced out Fed rate cuts – bringing markets closer to our expectations for rate cuts. We think the quick recovery in stocks highlights that one data release is not enough to spoil positive market sentiment for now. The Fed starting to cut rates and inflation nearing 2% should support stocks in the near term, but we stay nimble.

Global manufacturing and services activity is in focus this week, with global PMIs due for release, including for the U.S. and Europe. We look to the data as an early indication of Q1 GDP growth. We see interest rates in most developed markets remaining higher for longer than before the pandemic due to persistent inflationary pressures in the long term.

Week Ahead

Feb. 21: Euro area consumer confidence survey; Japan trade data

Feb. 22: Global flash PMIs

Feb. 23: Germany Ifo Business Climate Index

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 20th February, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

You are leaving medirect.com.mt

Please be aware that the external site policies, or those of another MeDirect website, may differ from this website’s terms and conditions and privacy policy. The next website will open in a new browser window or tab.

Note: MeDirect is not responsible for any content on third party sites, nor does a link suggest endorsement of those sites and/or their content.

We strive to ensure a streamlined account opening process, via a structured and clear set of requirements and personalised assistance during the initial communication stages. If you are interested in opening a corporate account with MeDirect, please complete an Account Opening Information Questionnaire and send it to corporate@medirect.com.mt.

For a comprehensive list of documentation required to open a corporate account please contact us by email at corporate@medirect.com.mt or by phone on (+356) 2557 4444.