Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Samara Cohen –

Chief Investment Officer of ETFs and Index Investments, Vivek Paul – Global Head of Portfolio Research, Paul Henderson – Senior Portfolio Strategist, and Laszlo Tisler – Portfolio Strategist all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Diversifying amid transformation: We see a transformation underway making a wide range of outcomes possible. That alters how we assess portfolio diversification and drivers of risk and return.

Market backdrop: U.S. stocks hovered near all-time highs last week. U.S. 10-year yields jumped sharply to near 4.40% before the Federal Reserve’s expected rate cut.

Week ahead: Even if the Fed cuts further in 2025, markets have come around to our view that sticky inflation means policy rates will settle well above pre-pandemic levels.

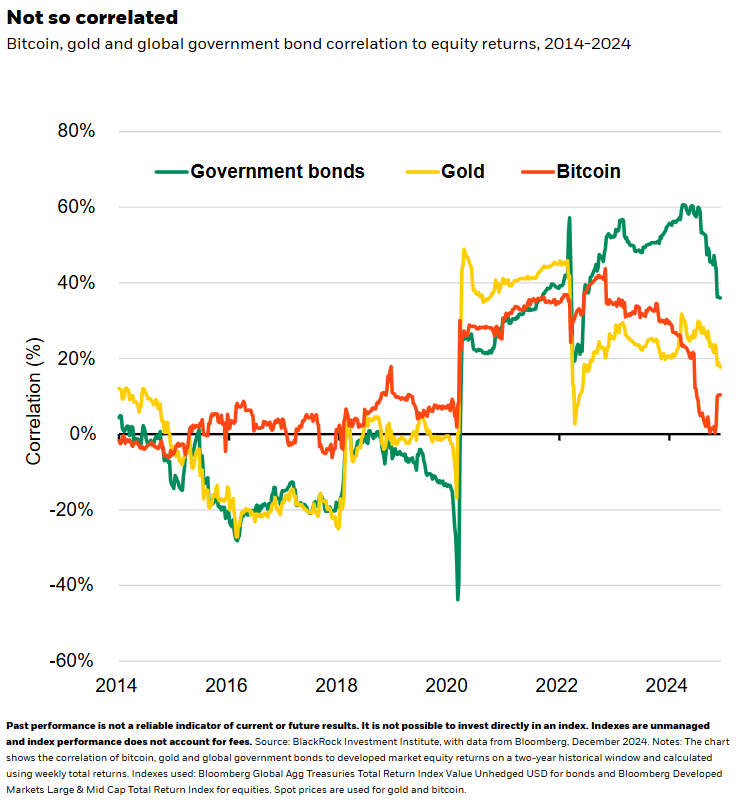

We believe economies are undergoing a transformation that could keep shifting the long-term economic trend. That creates a wide range of potential outcomes and a need to use scenarios to guide portfolio construction, we think. Government bonds have become a less reliable cushion against risk asset selloffs in this new regime. So investors should consider new diversifiers like gold and bitcoin – not to replace bonds, but to get exposure to distinct drivers of risk and return.

To help track the wide range of possible outcomes, we and BlackRock portfolio managers created five scenarios to map different market and economic outlooks over the next six to 12 months. Of the two scenarios where stocks sell off, we expect government bonds to provide protection in only one. Why? The long-negative correlation between stock and bond returns varies with the macro backdrop. It has turned positive amid sticky inflation – see the chart – so bonds less reliably cushion portfolios against equity selloffs. We eye other diversifiers since historical options don’t work as well. Take gold and bitcoin. Their correlation to global stocks remains limited, even with the occasional spike, making them better diversifiers than bonds in the last two years. This isn’t about replacing bonds: Today, gold and bitcoin don’t have the negative correlation bonds did but instead offer distinct sources of return.

We think gold has diversification properties because its risk and return drivers are different than those for equity and bond returns. Investors have long turned to gold to protect their portfolios from inflation and geopolitical risks, and to act as a store of value because its limited supply preserves value over time. Gold prices have surged this year alongside the U.S. dollar – a break from their traditional inverse relationship. What’s behind that? Investors seeking to protect portfolios against higher inflation, and some central banks seeking alternatives to major reserve currencies against the backdrop of heightened geopolitical tensions. Such demand can drive returns for alternative diversifiers like gold, no matter past correlations.

The case for bitcoin

Like gold, bitcoin could appreciate over time when its predetermined supply is met with growing demand. But demand for bitcoin is based on investor belief in its potential to be more widely adopted – and is thus central to its investment case. Some potential drivers of adoption: Bitcoin is decentralized, with no direct government ability to change supply. It’s also perceived to be immune from the effects of persistent government budget deficits, rising debt and higher inflation eroding the value of sovereign currencies. We see these factors making bitcoin more attractive in today’s world, and it could be a more diversified source of return because its value drivers are different than for traditional assets. Yet it remains highly volatile and vulnerable to sharp selloffs. And its value could tumble if it’s not widely adopted. Read more in our new paper (for professional investors).

We stay pro-risk headed into 2025 and think the most likely near-term scenario is one where U.S. growth moderates, but corporate profits remain strong. Risks to our view include surging long-term bond yields and greater trade protectionism. Our scenarios outline other risks, such as sticky inflation spurring central banks to stop cutting rates or slowing growth. If such an outlook spurs markets to flip-flop in their pricing of interest rates, bonds may not effectively hedge against any stock selloffs. We think investors should broaden their diversification toolkits, with gold and bitcoin potentially promising additions.

Our bottom line

Bonds no longer reliably diversify portfolios across a wide range of possible outcomes and scenarios. That calls for a rethink of diversifiers. This is our last weekly commentary of 2024, and we will return on Monday, Jan. 6. Happy holidays.

Market backdrop

U.S. stocks paused near all-time highs last week, with the S&P 500 up nearly 30% this year. U.S. core CPI for November cleared the way for a Federal Reserve rate cut this week but showed sticky services inflation, we think. U.S. 10-year Treasury yields rose more than 20 basis points to near 4.40% as the Fed could signal a pause in its cuts. Chinese 10-year bond yields fell the most since the 2020 Covid-19 outbreak on concerns expected stimulus may not be enough to revive growth.

Several central banks meet this week, with an expected Fed policy rate cut looming largest. U.S. core PCE, the Fed’s preferred inflation measure, out later in the week will show whether services inflation remains sticky. Wage growth is holding at levels that don’t suggest inflation is set to cool back near the Fed’s 2% target. These are key reasons why, even if the Fed is likely to cut rates further in 2025, we see rates ultimately settling higher than pre-pandemic levels.

Week Ahead

Dec. 16: Global flash PMIs

Dec. 18: Federal Reserve policy decision; UK CPI

Dec. 19: Bank of England policy decision

Dec. 20: U.S. PCE; Bank of Japan policy decision; Japan CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 16th December, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.