Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Axel Christensen – Chief Investment Strategist for Latin America and Laurent Develay – Head of Emerging Markets Local Debt, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Selective opportunities: The U.S. equity pullback has narrowed the performance gap with the rest of the world. We see bright spots in global markets benefiting from structural shifts.

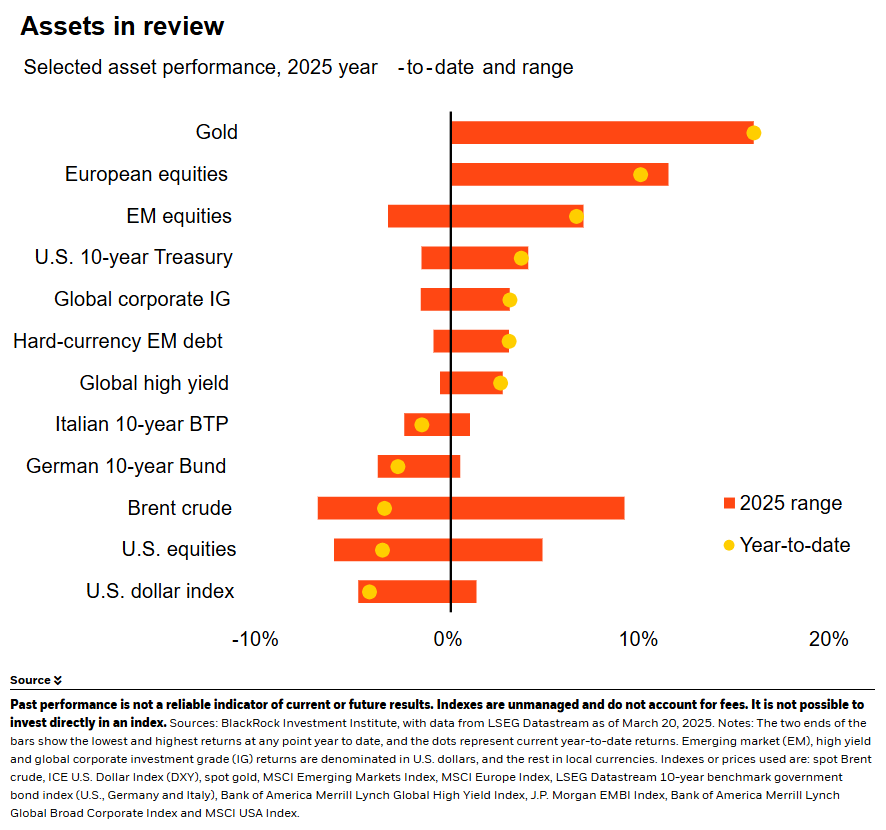

Market backdrop: U.S. stocks steadied after a four-week losing streak last week. Global stocks rose, with Japan the standout. U.S. 10-year Treasury yields ticked down to 4.25%.

Week ahead: Global PMI data could indicate any damage from U.S. policy uncertainty. We expect U.S. PCE data to keep showing that inflation is likely to settle above 2%.

The U.S. equity pullback has put a dent in U.S. outperformance over the rest of the world. We stay overweight U.S. stocks and see opportunities across global stocks. Europe’s fiscal boost may benefit some sectors. In Asia, corporate reforms have lifted Japanese stocks, while some Latin American countries tap into mega forces. Stronger currencies may boost the appeal of emerging local currency debt. Yet we think prolonged U.S. policy uncertainty could dim some of these bright spots.

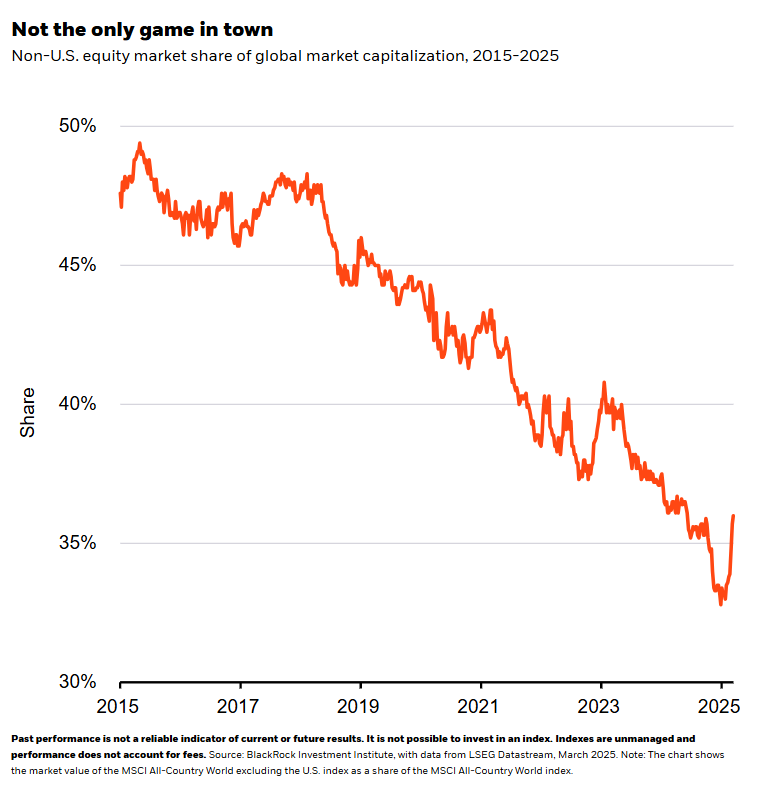

The weight of non-U.S. equities in global equity indexes has been on the rise since the end of January. See the chart. What’s driving that? In the near term, policy uncertainty has shaken investor conviction in U.S. growth and equity strength. That’s pulled the S&P 500 down more than 3%. The selloff has been exacerbated by investors rapidly pulling out of popular trades – like the tech-heavy momentum equity style factor and cyclical trades that were betting on a boost from growth from potential U.S. deregulation and tax cuts. Meanwhile, country-specific developments are boosting the appeal of global stocks, such as Germany’s big fiscal spending, Japan’s corporate reforms and Mexico’s role in rewiring supply chains. We think U.S. stocks can ultimately keep leading as the artificial intelligence (AI) theme broadens. Yet prolonged uncertainty poses a risk to both U.S. and global risk assets.

Germany’s defense and infrastructure spending plans were approved faster and with a greater scope than expected last week, not long after the federal election in February. Europe’s fiscal boost could lift revenues at aerospace and defense companies. Profit margins for the financial sector, our year-long preference, look set to grow as policy rates likely stay above pre-pandemic levels. Capital spending on electrification, energy efficiency and data centers could fuel growth for industrials. We’re selective as it will take time to see fiscal spending filter into the economy given the constraints in quickly boosting defense and infrastructure investment, on top of the limited fiscal room in most of Europe. European equity valuations still look attractive even as the discount versus U.S. stocks has narrowed from the 40% extremes seen last year, LSEG data show.

Mega forces at play

In Asia, structural shifts are spurring divides even within markets – reinforcing the need to be selective. A flood of apparently more efficient Chinese AI models has driven the Hang Seng index of mainland shares, full of big China tech companies, up 20% this year. That contrasts with the onshore benchmark CSI 300, roughly flat this year, showing how the AI theme in China has been centered in tech as it initially was in the U.S. Japan’s ongoing corporate reforms and mild inflation have driven long-lagging corporate return on equity, or profitability, to four-decade highs, LSEG data show – keeping us overweight stocks.

Latin America offers other bright spots. Mexico’s stocks have jumped nearly 8% year to date as the impact of U.S. tariffs has been less severe than expected. The Bank of Mexico’s cautious rate cuts have also helped stabilize the peso, up 4% against the U.S. dollar this year. While the impact of U.S. policy remains uncertain, Mexico is increasingly an intermediate trading partner between competing economic and geopolitical blocs. Chile’s equities have jumped 12% this year and its currency is up 8% against the dollar – given resilient economic growth and expected private investment in minerals key to the energy transition. More broadly, stronger EM currencies – if sustained – could brighten the appeal of EM debt issued in local currencies. We eye any temporary weakness due to trade uncertainty as an opportunity to upgrade the asset class to neutral.

Our bottom line

Country-level shifts and events are creating bright spots in global stocks, so we get selective. We stay overweight U.S. stocks on a six- to 12-month tactical horizon. Yet prolonged uncertainty could hurt both U.S. and global risk assets.

Market backdrop

U.S. stocks steadied after a four-week streak of losses. European stocks rose 0.5% last week, while Japan’s Topix was the standout, rising 3.3%. U.S. 10-year Treasury yields fell 6 basis points to 4.25%. We think the slide in U.S. equities was overdone as economic conditions don’t point to recession and corporate earnings hold up. But the longer uncertainty goes on, the more growth may suffer. We eye the “reciprocal” U.S. tariffs due to be announced on or before April 2 – and any fallout.

Global manufacturing and services survey results for March out this week could indicate how uncertainty from U.S. tariff policy is affecting economic sentiment around the world. We expect the U.S. PCE inflation data – the Fed’s preferred metric – to keep suggesting that inflation will settle above the Fed’s 2% target given still-elevated wage gains.

Week Ahead

March 24: Global flash PMIs

March 25: U.S. consumer confidence

March 26: U.S. durable goods; UK CPI

March 28: U.S. PCE

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 24th March, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.