Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Glenn Purves – Global Head of Macro and Nicholas Fawcett – Senior Economist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Sizing up the impact: Major U.S. policy changes have upped uncertainty in a world of structural shifts. We see a path where growth holds up and stay tactically overweight U.S. stocks.

Market backdrop: Global stocks slid last week after U.S. auto tariffs were announced and ahead of additional tariff details on April 2. U.S. 10-year yields were flat at 4.25%.

Week ahead: The U.S. administration is due to release details on “reciprocal” tariffs this week. We think the average U.S. effective tariff rate will ultimately settle near 10%.

Major U.S. policy shifts are exacerbating uncertainty and spurring policy responses globally, especially in Europe and Canada. It’s hard to gauge the ultimate macro and market impact given the various moving parts – with reciprocal tariffs a case in point this week. Yet when assessing possible impacts across policies, we see a path where artificial intelligence investment and potential deregulation could help boost economic growth. We stay overweight U.S. stocks over six to 12 months.

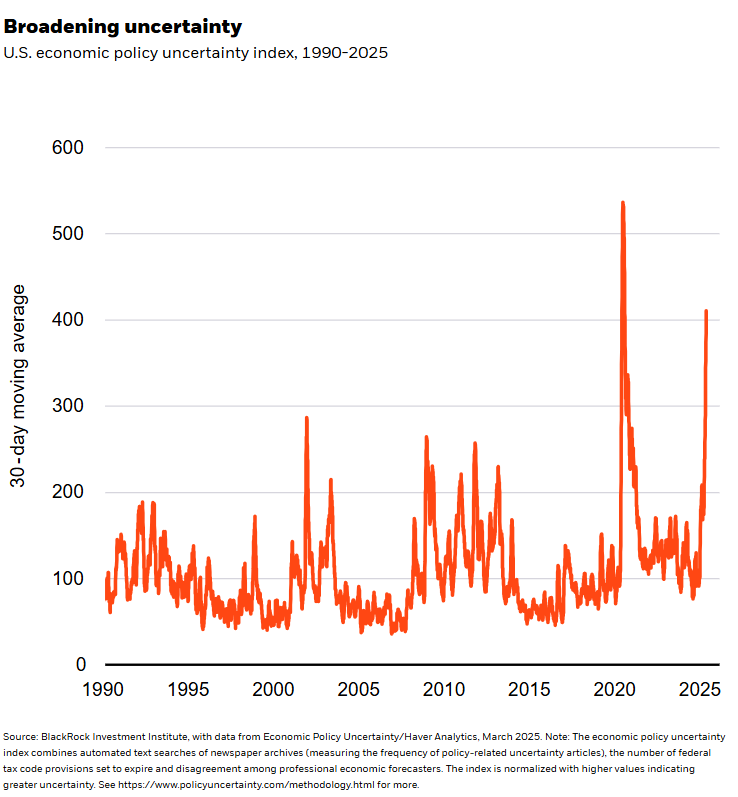

Long-standing global trade and foreign policy frameworks are being upended as the U.S. has raised tariff rates and catalyzed big policy responses elsewhere. Current levies on steel and aluminum, auto import tariffs revealed last week and details on “reciprocal” tariffs due April 2 are in focus now. We think the average U.S. effective tariff rate will settle near 10% – but it could take months to get there. Until then, we expect multiple changes to the mix of tariff rates. Investors have not faced this kind of trade uncertainty for decades and it has morphed into elevated economic uncertainty. See the chart. Unusually high policy uncertainty is driving a wedge between data based on sentiment surveys and data based on actual activity: U.S. consumer confidence hit a four-year low in March, even as activity holds up.

We think policy uncertainty will ease over the next year. Yet prolonged uncertainty increases the risk weakening sentiment hurts growth. At this stage, it’s hard to forecast the policy outcomes with any confidence given many moving parts and competing objectives. We think it’s more useful to assess the orders of magnitudes across different policy outcomes and how they could be reconciled: We assess growth, inflation and deficit impacts across trade, fiscal and immigration policy using a range of external estimates. On trade, we think tariffs are set to be a permanent feature of U.S. trade policy and a tool to raise revenue. While some external estimates see $300 billion in annual revenue from tariffs, they will likely push up on inflation and weigh on growth. The government is also aiming to cut costs to save around $1 trillion per year but nearing that would mean deep cuts to major federal programs. External estimates project only up to $300 billion of savings each year.

Assessing the policy mix

Yet those revenue gains could be offset by proposed policies that imply lower government revenues. The U.S. administration has proposed a continuation of the 2017 Tax Cut and Jobs Act that set out tax cuts for individuals and businesses and is due to expire in 2026. A continuation would widen the fiscal deficit by up to $450 billion, the Congressional Budget Office and Joint Taxation Committee project, while also providing a small boost to growth and inflation. The administration has also made it a priority to reduce net immigration. If immigration slows back to pre-pandemic levels, currently elevated wage pressures would likely persist, GDP growth would slow slightly, and tax revenues would fall a little.

We expect this policy mix to reinforce persistent inflation pressures and higher long-term yields – and leave the fiscal deficit above 5% looking out to 2030. What matters for risk assets amid higher rates: whether growth can hold up. We see a path where it could if the AI growth boost of the past two years persists and if deregulation spurs an additional boost. We think U.S. stocks can resume their global leadership due to resilient growth and mega forces – like AI. We stay underweight long-term U.S. Treasuries, favoring short- and medium-term bonds.

Our bottom line

U.S. policy shifts have conflicting economic impacts. We see a path for resilient growth and mega forces to support U.S. equities, keeping us overweight tactically. We stay underweight long-term bonds, preferring shorter-term bonds.

Market backdrop

The S&P 500 slid 1.5% last week before the April 2 U.S. tariff announcement. Europe’s Stoxx 600 fell more than 1% last week, in part reflecting the news of U.S. tariffs being levied on global auto imports. But Europe is still outperforming this year, with gains of nearly 7% compared with the S&P 500’s 5% drop. U.S. 10-year Treasury yields ended the week flat at 4.25%, falling back from one-month highs after soft U.S. consumer spending data for February.

This week all eyes are on the U.S. administration’s planned April 2 date to release more details about “reciprocal” U.S. tariffs that match many of those imposed on U.S. products by other countries. The much higher rates currently planned for Mexican and Canadian imports and on autos globally could be cut after negotiations, while new ones could be introduced elsewhere. We think the average U.S. effective tariff rate will ultimately settle near 10%, the highest since the 1940s.

Week Ahead

April 1 : Japan Tankan business condition survey; euro area flash inflation

April 2 : Additional U.S. tariff details

April 3 : China Caixin services PMI; U.S. trade data

April 4 : U.S. payrolls data

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 31st March, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.