Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Glenn Purves – Global Head of Macro and Catherine Kress – Head of Geopolitical Research, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

U.S. tariff pause : The consideration of some financial risks and costs of tariffs has put a check on the U.S. approach. We extend our tactical horizon to dial up risk-taking.

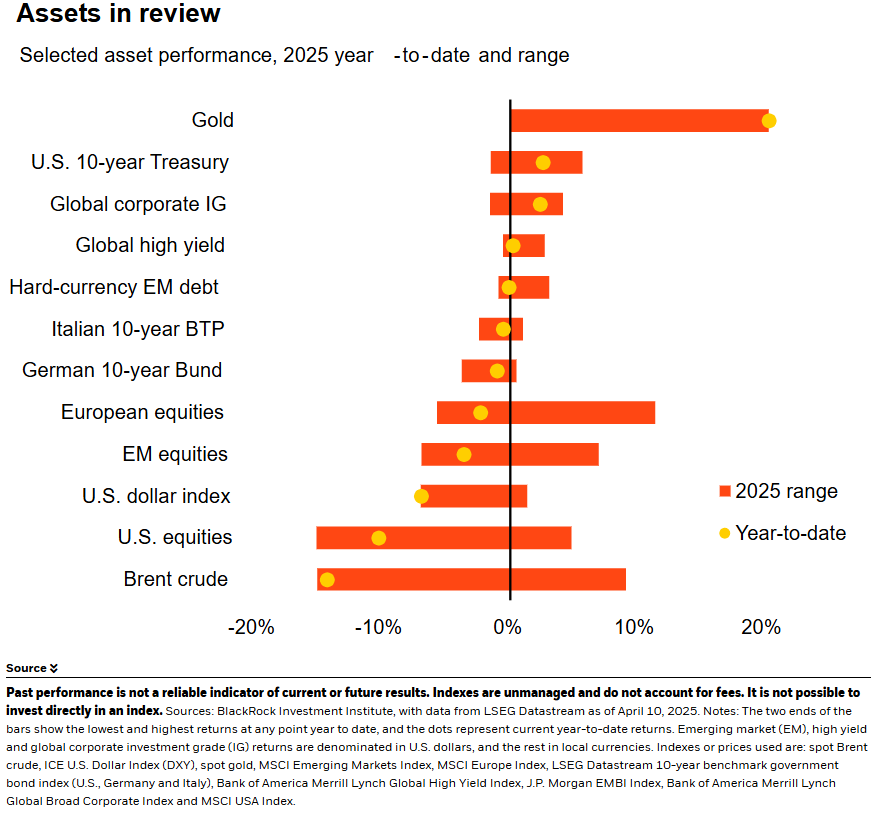

Market backdrop : Global markets endured extraordinary volatility last week. A spike in long-term U.S. Treasury yields was one factor seeming to drive a change in tactics.

Week ahead : We expect the European Central Bank to cut interest rates this week. U.S. tariffs will likely lower growth in Europe, but greater fiscal spending may limit the drag.

The 90-day pause of tariffs on most countries and exemption of key tech imports suggest the U.S. administration is taking some account of financial risks and costs as well as a country’s willingness to engage. It shows there are factors that could put a check on the administration’s maximal tariff stance. As a result, late last week we extended our tactical horizon back to six to 12 months to dial up risk. Yet we still think tariffs can hurt growth and lift inflation, and major uncertainty remains.

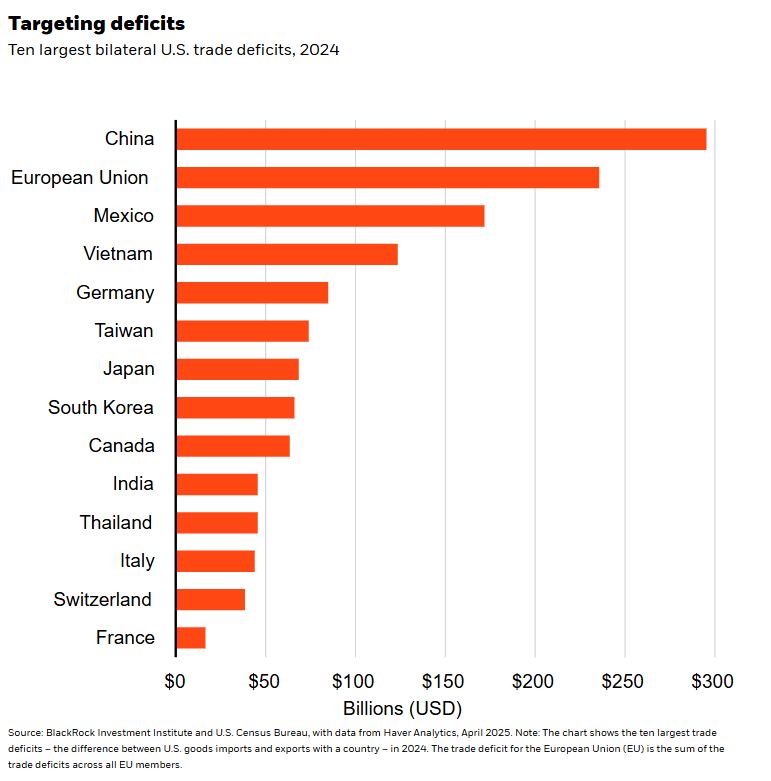

The U.S. has paused country-specific “reciprocal” tariffs on all nations, except China, for 90 days and exempted some key tech imports. These tariffs are intended to create negotiating leverage on countries with which the U.S. runs goods trade deficits – and reduce imbalances. See the chart. Even with the pause, the U.S. average effective tariff rate is still around 20%, including 145% tariffs on select Chinese imports. We see U.S. tariffs adding to inflation. Prolonged uncertainty raises the risk of recession. It may drag on corporate investment and delay longer-term commitments. Consumer spending could be hurt by any erosion of wealth and real incomes. Dented confidence in the U.S. could curb foreign investor appetite for U.S. assets. Trade tensions with China are set to deepen. We see tariffs lowering growth in China, and potential policy stimulus only partly offsetting that drag.

Along with country-specific tariffs, we see two other primary types of U.S. tariffs. First, tariffs on strategic sectors to support reshoring of activity. Second, a universal 10% tariff on most imports to generate revenue and aid domestic production. Even with last week’s pause – and subsequent exemption of some key tech imports such as smartphones – the U.S. is still facing much higher tariffs than we expected a few weeks ago. With uncertainty around where tariffs will land and unpredictable negotiations ahead, we aim to understand the factors that can prompt the administration to change course on policy. It appears to be taking some account of market volatility, financial risks and other sources of pushback, as well as a country’s willingness to engage. That is putting a check on its maximal stance and could bind policy changes.

Checks on policy emerge

The implications? The near-term risk of a financial accident has eased. We cautiously leaned back into risk late last week by extending our tactical horizon back to six to 12 months from three months. We also renewed our overweight to U.S. and Japanese stocks. U.S. equities are supported by the AI theme, resilient corporate earnings and a so far solid economy. We see Japanese stocks still benefiting from stronger corporate profits and shareholder-friendly reforms. We recently upped Europe’s stocks to neutral but focus on selective opportunities while looking for more progress on structural challenges.

Yet we expect ongoing risk asset volatility and potentially sharp reversals. Spiking yields in long-term U.S. Treasuries seemed to be a factor in the change in tariff tactics. We stay underweight long-term Treasuries, our highest conviction view: tariffs are likely to add to already sticky inflation, and congressional budget plans last week reinforce the outlook for persistent budget deficits. We favor gold instead as a portfolio diversifier. The broad-based equity selloff has created opportunities to tap into certain sectors, and selectivity is key. We still like U.S. technology benefitting from the AI buildout and adoption. We also favor global banks. That includes U.S. banks given the scope for deregulation even with some potential economic pain. We also like banks in Europe (higher rates versus pre-pandemic levels) and Japan (stronger loan growth).

Our bottom line

The U.S. paused most “reciprocal” tariffs even as U.S.-China trade tensions look set to deepen. Checks on policy allowed us to extend our tactical horizon back to six to 12 months and resume our positive view on U.S. and Japanese stocks.

Market backdrop

Markets have endured extraordinary volatility due to uncertainty over U.S. tariffs. The S&P 500 rebounded nearly 6% last week, with one of its largest daily jumps in its history after the pause on “reciprocal” tariffs. But the index remains 13% below its February record high. The U.S. dollar tumbled to three-year lows against major currencies even as both 10- and 30-year U.S. Treasury yields spiked about 50 basis points to 4.50% and 4.90% – on track for their largest weekly rise in four decades.

We expect the European Central Bank (ECB) to cut interest rates at its policy meeting this week. What seemed to be a toss up between a cut and a hold before the announcement of additional U.S. tariffs on April 2 will most likely be a cut, as sweeping tariffs risk pushing the bloc towards recession. We expect tariffs to lower growth in Europe, yet greater fiscal spending could limit the drag from tariffs.

Week Ahead

April 15 : UK unemployment

April 16 : UK CPI

April 17 : ECB policy decision

April 18 : Japan CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 14th April, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.