Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Glenn Purves – Global Head of Macro and Nicholas Fawcett – Senior Economist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

U.S. recession fears : Markets are doubting U.S. growth and equity strength. Yet economic conditions don’t signal a downturn. Resilient earnings keep us overweight U.S. stocks.

Market backdrop : Global stocks trimmed their losses last week. The S&P 500 was down 1% after briefly entering a technical correction as recession fears gripped markets.

Week ahead : We expect the Federal Reserve to hold rates steady at this week’s policy meeting. Markets have been pricing in deeper rate cuts due to fears about U.S. growth.

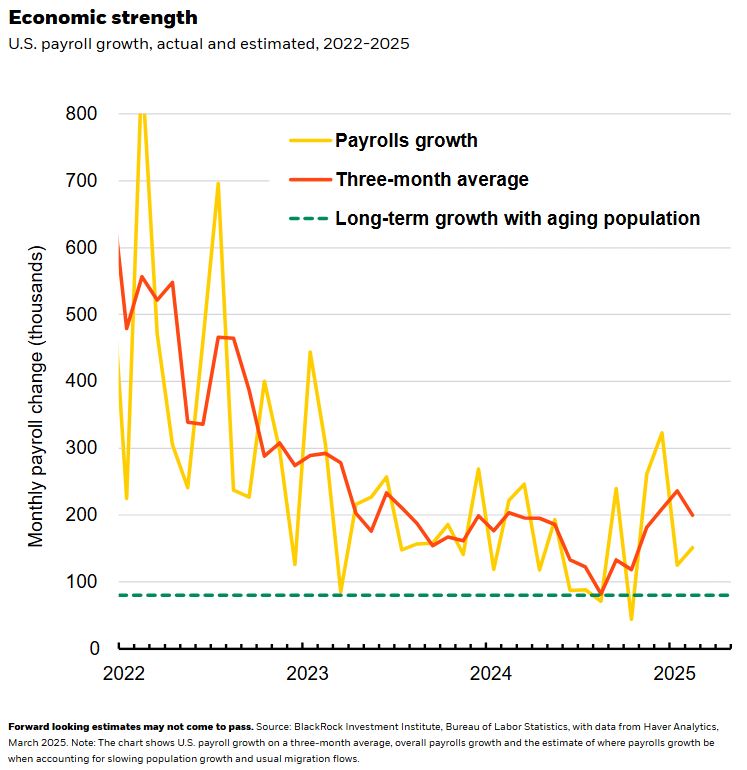

The S&P 500 has slid 8% from its February high and 4% this year as investors worry U.S. policy changes will bite growth that has been key to U.S. outperformance. Yet fundamental, quantitative economic data doesn’t indicate a downturn is near. Job gains have slowed since 2022 but remain above the long-term level we expect given an aging workforce. See the chart. U.S. corporate earnings expectations and high-frequency indicators of consumer health like weekly credit card spending are also solid, JPMorgan data show. Yet near-term risks to growth loom: Uncertainty could hit consumer spending, investment and trade. The longer policy uncertainty lasts, the more growth could suffer – but even that’s not certain. U.S. policy is spurring government spending elsewhere, reinforcing our view that developed market policy rates and bond yields will stay well above pre-pandemic levels.

Markets have also questioned U.S. equity strength, especially for the tech sector. U.S. recession fears reignited the selloff in tech stocks. The Nasdaq has fallen 11% from its all-time high hit in February – the biggest retreat since the 2022 equity selloff. Yet we stay overweight U.S. stocks on a six- to 12-month tactical horizon. Earnings expectations are healthy, with 12% growth forecast for the S&P 500 this year versus 14% last September, LSEG Datastream data show. Tech corporate margins, earnings and revenues forecasts are holding up and the sector still has the fastest expected growth this year. Free cash flow for the sector is also at 30% of total sales, the highest share since 1990 – a sign of current strength.

Allocating for uncertainty

Recent volatility has been exacerbated by policy uncertainty and investors moving out of crowded positions. For example, last week saw a rapid move away from popular trades, like the tech-heavy momentum equity style factor that had some of its sharpest declines since the pandemic. Both could drive more volatility in the near term. But, over time, deleveraging will have run its course and uncertainty will likely ease as we get more policy implementation details, such as the White House’s full tariff plan due in April. Then, some of the risk premium investors now want for extreme uncertainty could be priced out again.

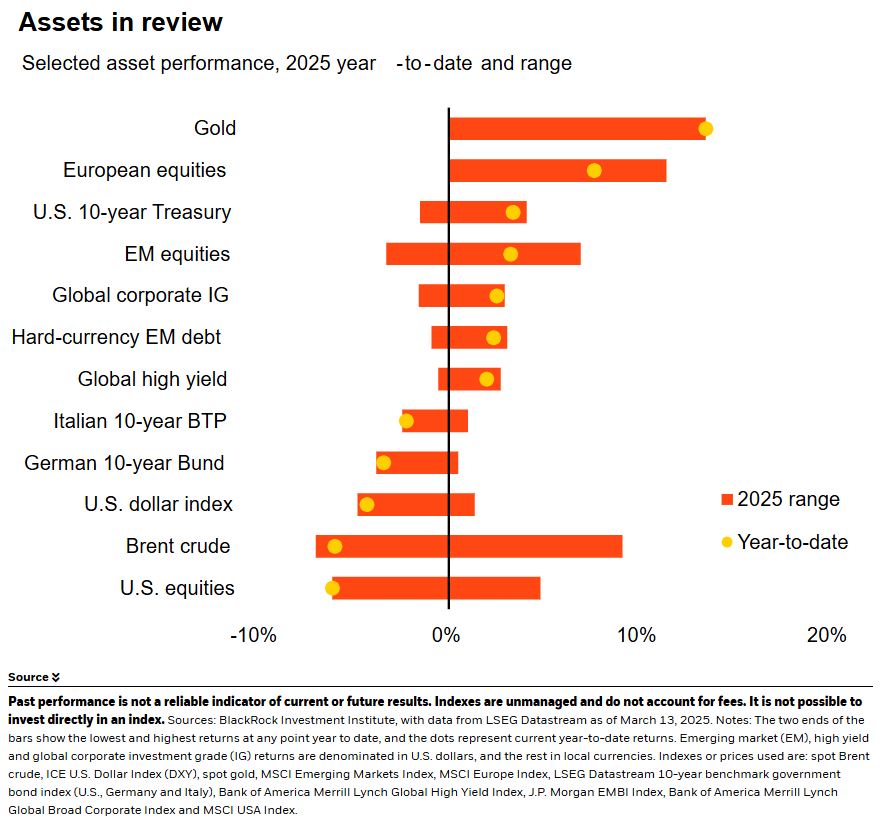

Long-term U.S. Treasuries have briefly buffered against the stock retreat. But their portfolio diversification role has weakened since the pandemic. We think yields can climb as investors demand more compensation, or term premium, for the risk of holding long-term bonds. Recent inflation data has been noisy, but core CPI is still above what’s consistent with the Federal Reserve’s 2% target. That limits how far the Fed will be able to cut. A likely rising U.S. fiscal deficit – even with revenue from tariffs and potential spending cuts – could also lead to higher term premium. In the past, investors saw long-term bonds as low risk even with heavy government debt loads because they believed low inflation and low interest rates were here to stay. But that fragile equilibrium has been disrupted. Germany’s plans to boost fiscal spending reinforce higher-for-longer rates – and bond yields – globally, we believe. We think gold could be a better diversifier than Treasuries in this environment.

Our bottom line

We think the biggest risk to U.S. growth is prolonged policy uncertainty. U.S. stocks could face more near-term pressure, but we stay overweight on our tactical horizon. We stay underweight long-term Treasuries as we see yields rising.

Market backdrop

Global equity markets trimmed their losses last week after the S&P 500 briefly entered technical correction territory Thursday, falling 10% from the February record peak. The S&P 500 rebounded on Friday to end the week down 1%, but it has slid 4% for the year near six-month lows as concerns about U.S. tariffs and a U.S. recession gripped markets. Ten-year U.S. Treasury yields were largely steady last week near 4.30% even with the equity selloff and lower-than-expected CPI inflation data.

All eyes are on the Federal Reserve policy meeting this week. We, like markets, don’t expect the Fed to cut at this week’s meeting. Yet markets have priced in about two to three 25 basis point rate cuts this year, versus expectations for just one earlier this year. We think this reflects U.S. recession fears even though economic condition don’t point to a downturn. Even if prolonged uncertainty hurts growth, we still see persistent inflation limiting how much the Fed can cut.

Week ahead

March 19 : Fed policy meeting

March 20 : Bank of England (BOE) policy meeting

March 21 : Japan CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 17th March, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.