Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Helen Jewell – Chief Investment Officer EMEA, Fundamental Equities, Natalie Gill – Portfolio Strategist and Carolina Martinez Arevalo – Portfolio Strategist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Tech talk: We think major tech firms can keep delivering on high corporate earnings expectations. We stay positive on stocks and the artificial intelligence theme.

Market backdrop: U.S. stocks retreated last week, led by technology names. We expect some bouts of volatility ahead over the short term. Stocks of smaller-sized firms rose.

Week ahead: We’re eyeing how a surprisingly soft U.S. CPI report translates into PCE data. We think cooling inflation means the Fed can start cutting rates in coming months.

A tech-driven pullback has hit stocks this month as investors piled into segments like smaller companies on hopes for cooling inflation and Federal Reserve interest rate cuts. Looking through this near-term noise, we think tech will drive returns as consensus expects big tech companies to carry positive earnings results for the market. We see pullbacks as an opportunity to lean into stocks. We stay overweight the AI theme and U.S. stocks as we watch for the AI buildout to boost other sectors.

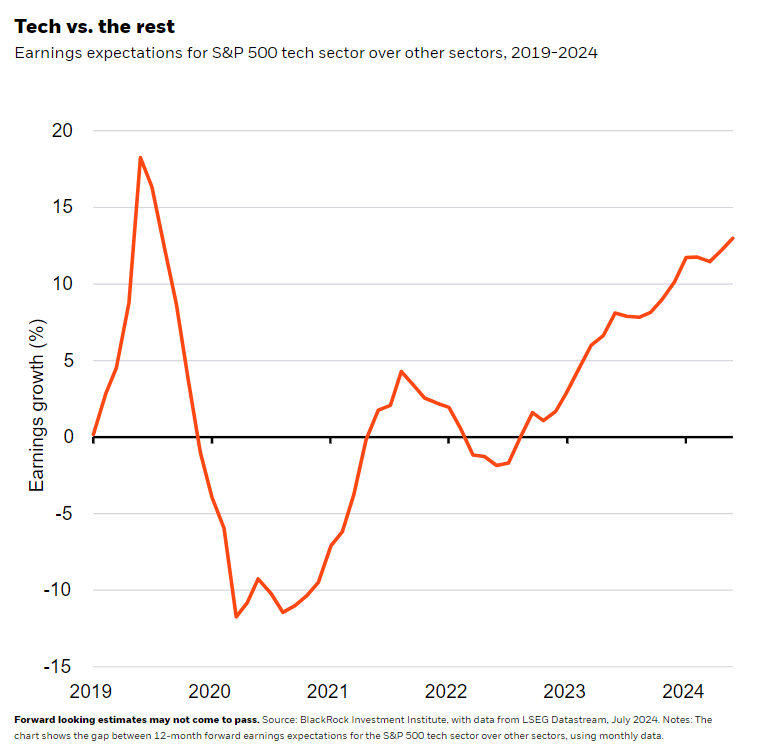

Tech stocks have led the U.S. equity retreat from record highs, reached on hopes for big tech companies to keep beating high earnings expectations thanks to the AI theme. Stocks for debt-laden and interest rate-sensitive small companies surged 3.7% after the soft June CPI data reignited market hopes for quicker Fed rate cuts. We expect this rebound to be short lived as central banks likely hold rates higher for longer given persistent inflation pressures. Rather than the macro, we think the market is being driven by structural shifts like AI that are spurring a transformation. We’re monitoring the impact on Q2 earnings. Why? Consensus forecasts for tech earnings have risen well above those for the rest of the S&P 500. See the chart. That’s still playing out: Analysts see tech earnings growing 18% year over year in Q2 versus 2% for the rest of the index, LSEG Datastream data show.

Such forecasts set a high bar for tech companies to keep delivering on earnings. We think they can, but more volatility could be ahead with Nvidia’s highly expected results due in late August. We especially see sudden pullbacks during the northern hemisphere summer, when reduced trading activity can exacerbate market volatility. The tech sector could also suffer if investors worry earnings growth won’t justify big capital spending on AI. Those worries likely contributed to the share drop for major chipmakers – on top of news of potential U.S. efforts to further limit foreign access to chips. Any trade or regulatory policy changes after the U.S. election in November that restrict the AI buildout could hurt tech, too. U.S. President Joe Biden’s announcement over the weekend that he will drop out of the presidential race may add to volatility, although pressure had been building in recent weeks. We monitor these risks while staying overweight the AI theme – and for now see sudden pullbacks as an opportunity to dial up risk-taking. This environment requires a new investment playbook.

Looking beyond tech

The earnings lead for the tech sector could narrow later this year as analysts expect earnings to improve in other sectors. We see the buildout of AI boosting sectors such as industrials, materials, energy and healthcare as it helps drive a transformation potentially on par with past technological revolutions. We don’t believe the rally in U.S. small capitalization stocks is part of this eventual earnings improvement. They are more sensitive to higher interest rates and not exposed to the drivers of the transformation we expect. Case in point: U.S. small caps have suffered five quarters of shrinking earnings due to higher rates.

Regionally, we see selective opportunities in Europe as lower interest rates support growth and already improving earnings. At the sector level, we were more positive on banks earlier in the year given their resilient balance sheets. Relative valuations now look pricier. We prefer construction, utility and semiconductor companies that benefit from rate cuts and mega forces. We also went overweight UK stocks because post-election political stability and recovering growth could boost valuations.

Bottom line

We lean against the market extrapolating too much from a single data release like the CPI. We expect big tech firms to keep driving equity returns. We stay overweight U.S. stocks and the AI theme.

Market backdrop

U.S. stocks pulled back from record highs last week. Technology names led the retreat, driven by concerns over potentially stronger restrictions on semiconductor exports to China. A global IT outage stoked further unease. We expect some bouts of volatility ahead, as reflected in the surge in small cap shares. U.S. 10-year Treasury yields edged up on the week – showing that investors were not viewing this equity rotation and volatility as a pure risk-off episode, in our view.

We’re watching July U.S. PCE data – the Fed’s preferred inflation measure – to see if the decline in CPI services inflation is repeated. June saw core services inflation, excluding housing, fall for a second month straight. We think the recent slowdown in services inflation is not consistent with current wage gains. We still expect the Fed to cut rates in 2024, but to levels higher than pre-pandemic.

Week Ahead

July 23: Euro area consumer confidence

July 24: Global flash PMIs

July 25: U.S. GDP and durable goods data; Japan service PPI

July 26: U.S. core PCE; Tokyo CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 22nd July, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.