Jean Boivin, Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Alex Brazier – Deputy Head and Vivek Paul – Global Head of Portfolio Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Lessons learned: We think 2023 stressed the value of adapting to a new volatile macro regime, and leveraging investment insight and structural forces to find opportunities.

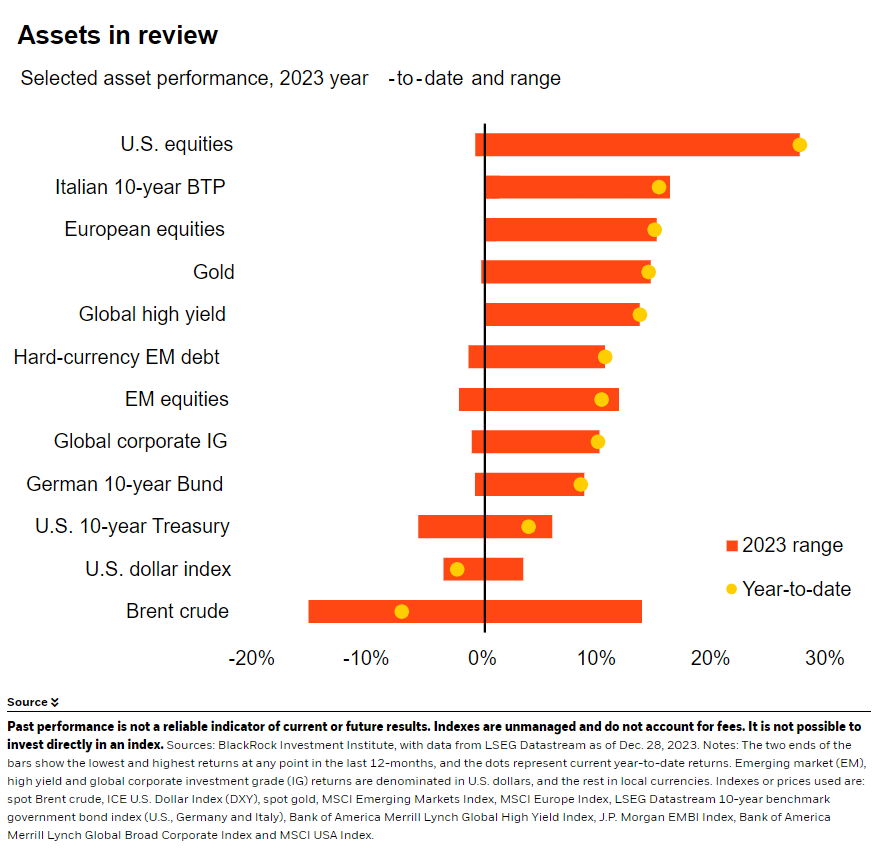

Market backdrop: U.S. stocks surged in 2023, a reversal from their 2022 underperformance. Flip-flopping market views about the policy path stoked volatility in long-term bonds.

Week ahead: December U.S. jobs data out this week should signal how much more the labor market needs to normalize. Slower jobs growth is a long-term supply constraint.

We take three lessons from 2023 to shape our investment approach in the new year. First, markets flipflopping between macro narratives does not reveal new information about where we will end up. This is not a typical business cycle and context is everything. Second, greater dispersion is creating opportunities. That requires skill and granularity. Third, artificial intelligence buzz has underpinned U.S. stock performance – and shows mega forces matter now, not just in the future.

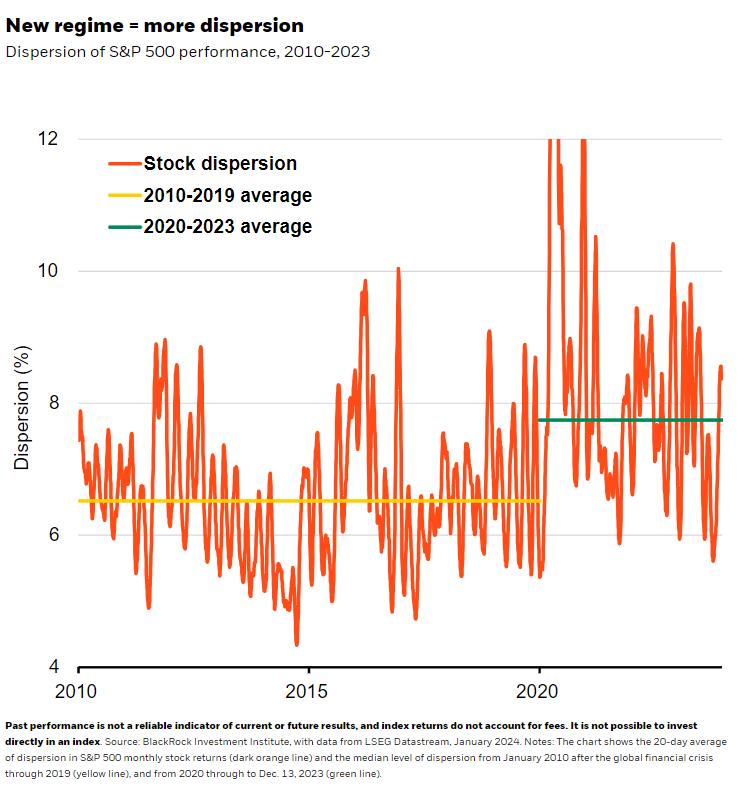

Looking back, 2023 largely saw a concentrated tech stock rally, with the Nasdaq up 55% from 2022. A market-wide rally since November also supported tech and led the equal-weighted S&P 500 to eke out a 12% return. Overall, we are seeing more dispersion in individual stock returns since 2020 (green bar in the chart). Macro uncertainty, geopolitics and structural shifts are driving volatility and dispersion. We think markets have stoked volatility, too, by viewing the new regime through the lens of a typical business cycle. Investors leaned into long-term bonds in early 2023 on hopes the Federal Reserve would cut policy rates by year end. It then became clear higher government spending and labor shortages are set to make inflation persistent and keep interest rates above pre-Covid norms. Ten-year Treasury yields surged to 16-year highs near 5% in October as markets priced in this outlook. They tumbled back below 4% by year end after the Fed blessed the pricing of rate cuts.

These volatile moves underscore the first lesson that was reinforced in 2023: The macro backdrop is much more uncertain today than during the Great Moderation period of stable growth and inflation. This is tough to navigate for markets, with them flipflopping between macro narratives through 2023. In the final quarter alone, both stocks and bonds surged on news of lower inflation – with the November PCE report confirming a goods-led slowdown – and dovish Fed projections. Small caps rallied on hopes for a soft economic landing. And markets have repeatedly priced in aggressive rate cuts just to walk them back. All this shows markets may extrapolate a lot from one piece of data or central bank comment. That’s taking a big bet on the macro outlook when the range of outcomes is wide, in our view. We don’t believe the prevalent market narrative tells us new information about where the macro will end up. Yet we are cognizant markets can run with a narrative for some time. This is why we turned tactically neutral on long-term U.S. Treasuries last October. We think long-term yields will resume their rise over time as investors demand more compensation amid persistent inflation and budget deficits.

Our second lesson

The greater macro risk means the dispersion of returns has increased. The result: a wide divergence in performance across equity sectors – and greater opportunities for investment expertise to shine, in our view. The correlation between bond and stock returns has flipped firmly into positive territory, meaning stocks and bonds fall or rise simultaneously. As a result, the old approach to portfolio construction that relied on bonds to offset equity sell-offs won’t work, in our view. Instead, we advocate breaking up broad asset allocation blocks and digging deeper. All this is why our second lesson is that granularity is more essential now. We look beyond the macro to seek above-benchmark returns, or alpha, by being dynamic and selective.

Our third lesson

One example of going beyond broad asset class exposures is to harness mega forces. The artificial intelligence (AI) mega force drove 2023 stock performance to an even larger extent than we had imagined. The importance of AI and other mega forces hammers home our third lesson: Structural forces matter now. Aging populations mean an ever-rising share of the population is past retirement age, resulting in worker shortages. That’s a key constraint fueling U.S. inflation now as a tight labor market keeps wage growth elevated. Others include the low-carbon transition and geopolitical fragmentation. The latter is evidenced by wars in Ukraine and Gaza and the intensifying structural competition between the U.S. and China.

Our bottom line

2023 emphasized the macro risks but also the opportunities on offer from structural shifts and getting granular in the new regime. Our 2024 Global Outlook outlines how we capture them.

Market backdrop

U.S. stocks surged roughly 25% last year, a near mirror image of their downtrodden 2022 performance. That was partly driven by excitement over AI lifting tech stocks and carrying the broader market. Meanwhile, the 10-year Treasury yield ended the year where it started: It climbed from lows of roughly 3.3% in April, to 16-year highs near 5% in October before falling below 3.9% at year end. We think some of the sharp swings in narratives – and markets – reflect the new regime of greater volatility.

We will be looking to the U.S. payrolls data for December out this week to gauge how much further the labor market has left to normalize in the new year after the pandemic. Structurally slower labor force growth is one of several long-term production constraints we think will prevent the U.S. and many other major economies from growing at their pre-pandemic pace without sparking renewed inflation.

Week Ahead

Jan. 3: U.S. ISM manufacturing PMI

Jan. 4: China Caixin services PMI

Jan. 5: U.S. payroll data; euro area inflation

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 2nd January, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.