Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Glenn Purves – Global Head of Macro Research and Bruno Rovelli – Chief Investment Strategist

for Italy all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Three triggers : We are pro-risk to start 2025. Yet we’re ready to evolve our view if policy shifts, corporate earnings and financial market cracks spell a deteriorating outlook.

Market backdrop : U.S. stocks slid and 10-year U.S. Treasury yields climbed near 4.80% last week after a strong U.S. jobs report. UK gilt yields jumped on fiscal outlook concerns.

Week ahead : We get U.S. CPI this week. Robust wage growth and sticky core services inflation should keep broad inflation from falling to the Federal Reserve’s target, we think.

We are pro-risk, with the biggest overweight in U.S. stocks, yet eye three areas that could spur a view change. First, we’re watching policy, notably how U.S. tariffs and fiscal policy shape up. Second, we watch whether investor risk appetite will sour due to corporate earnings and lofty tech valuations amid the artificial intelligence (AI) buildout. Third, we look for elevated vulnerabilities, like surging bond yields as markets price out rate cuts and corporate debt refinancing at higher interest rates.

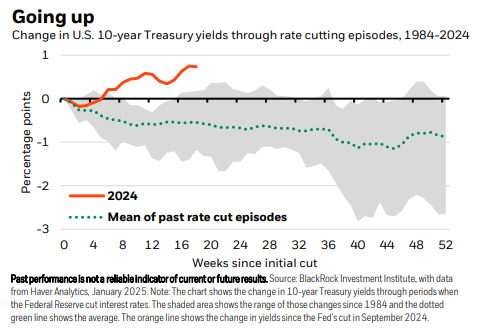

We upped our U.S. equities overweight in December as we expected AI beneficiaries to broaden beyond tech given resilient growth and Fed rate cuts. We think U.S. equity gains could roll on. Yet an economic transformation and global policy shifts could push markets and economies into a new scenario from our 2025 Outlook. We look through near-term noise but outline triggers for adjusting our views, by either dialing down risk or shifting our preferences. First, we’re tracking the impacts of global policy – especially U.S. trade, fiscal and regulatory policy. Second, we gauge whether risk appetite will stay upbeat as earnings results for AI beneficiaries come in and given high tech valuations. Third, vulnerabilities like a sudden jump in bond yields could also shift our view. The unusual yield jump since the Fed started cutting rates underscores this is a very different environment. See the chart.

The first trigger to change our view is whether or not President-elect Donald Trump takes a market-friendly approach to achieve goals like improving growth and reducing budget deficits. In a market-friendly approach, rolling back financial regulation and cutting government spending could boost economic growth and risk assets. That, plus efforts to rebalance global trade and expand fiscal stimulus in countries where investment and consumer spending have lagged the U.S., may help address trade deficit worries. In a less market-friendly approach, plans to extend tax cuts alongside large-scale tariffs could deepen deficits and stoke inflation. More broad-based tariffs could strengthen the U.S. dollar, fuel inflation and call for high-for-longer interest rates. This plan would clash with Trump’s calls for a weaker dollar to boost U.S. manufacturing and his push for rate cuts. We look through noisy headlines around policy and focus on how policy changes take shape this year.

Sentiment and financial cracks

The second trigger: deteriorating investor sentiment due to earnings misses or lofty tech valuations. The “magnificent seven” of mostly tech companies are still expected to drive earnings this year as they lead the AI buildout. Their lead should narrow as resilient consumer spending and potential deregulation support earnings beyond tech. While earnings might surprise to the upside, any misses could renew investor concern over whether big AI capital spending will pay off and if high valuations are justified – even if we think valuations can’t be viewed through a historical lens as an economic transformation unfolds.

In our third trigger, we’re watching for elevated vulnerabilities in financial markets – including an already jittery bond market. We expect bond yields to climb further as investors demand more term premium for the risk of holding bonds. Term premium is rising from negative levels and is at its highest in a decade, LSEG Datastream data show. The surge in UK gilt yields shows how concerns about fiscal policy can drive term premium – and bond yields – higher. The refinancing of corporate debt at higher interest rates is another risk. It could challenge the business models of companies that assumed interest rates would remain low. But many companies have refinanced debt without defaulting since the pandemic given strong balance sheets.

Our bottom line

We see U.S. equity gains cooling from their highs this year but staying strong, while U.S. Treasury yields climb. We stay overweight U.S. stocks and underweight long-term Treasuries, yet we’re watching triggers to change our views.

Market backdrop

U.S. stocks fell more than 1% last week. Ten-year U.S. Treasury yields climbed near 4.80%, to a 14-month high and near their 2023 peak partly due to a surprisingly strong U.S. jobs report. The data suggest immigration is still making it possible to sustain larger job gains without adding to wage pressures. Yet wage gains are still strong enough for the Fed to keep policy rates higher for longer. UK 30-year gilts yields hit their highest in almost three decades on concerns about the UK fiscal path.

U.S. CPI is in store this week. We watch for whether inflation stays sticky in line with the recent trend. Wage growth and core services inflation remain at a level inconsistent with overall inflation falling back to the Federal Reserve’s 2% target, in our view. Longer term, we think labor supply constraints like population aging should keep inflation sticky, preventing the Fed from cutting policy rates much below 4% – much higher than pre-pandemic levels.

Week Ahead

Jan. 13: China trade data

Jan. 15: U.S. CPI; UK CPI

Jan. 16: UK GDP

Jan. 10-17: China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 13th January, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.