Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Simon Blundell – Head of European Fundamental Fixed Income and Michel Dilmanian – Portfolio Strategist all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Tackling headline risk: Shifting U.S. policy and the evolving artificial intelligence (AI) story highlight the risks markets face in 2025. We stay risk on and keep our U.S. equity overweight.

Market backdrop: U.S. stocks were flat last week. Stocks recovered from the tariff-driven volatility thanks to solid Q4 corporate earnings, led by tech. U.S. bond yields dipped.

Week ahead: The January U.S. CPI is due this week. Wage growth remains above the level that would allow inflation to fall back to the Federal Reserve’s 2% target, we think.

U.S. policy shifts and AI advances have driven sharp market volatility so far this year. This volatility underscores the fact we are in a new macro environment, with a wider range of outcomes possible. We stick to our core risk-on framework yet fine-tune our views. We stay overweight U.S. equities on a solid macro outlook and the AI mega force – a big, structural shift. We go overweight government bonds in the euro area, where the potential growth hit from tariffs should reinforce rate cuts.

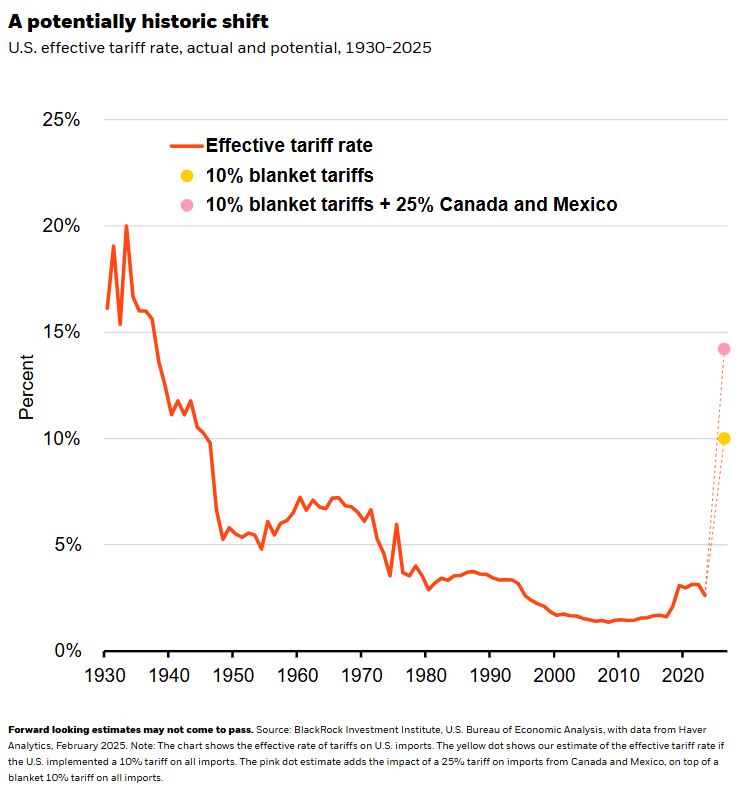

We entered 2025 expecting the unexpected and for policy to add volatility. That has played out. Bond yields spiked on fiscal concerns, then fell on growth fears and the U.S. Treasury’s pledge to lower them. China startup DeepSeek’s seeming AI breakthrough and U.S. tariff news have also stoked volatility. We think tariffs will be a key U.S. policy tool. The U.S. could pursue universal tariffs as a tax this week, with reports suggesting they could come as reciprocal tariffs matching those placed by other countries. We eye potential universal tariffs on a reciprocal basis or at a flat rate, such as 10%, with tariff levels of 25% serving as a negotiating tool. That could push the U.S. effective tariff rate near 1930s levels. See the chart. The macro impact of tariffs depends on their level, scope, duration and any retaliation. The risk of higher inflation and lower growth likely keeps the Federal Reserve on hold for now.

U.S. equities have proved resilient this year, though escalating trade tensions could keep the pressure on in coming months. We think they can keep doing so, even with rolling tariff headlines and the potential for 10% blanket tariffs – provided growth holds up and inflation stays in check. Resilient growth, solid corporate earnings, potential deregulation and the AI theme keep us upbeat. Q4 earnings growth has broadened as we expected, with S&P 500 earnings excluding the “magnificent 7” stocks up about 5% from a year ago and the consensus eyeing a 10% rise this year, LSEG Datastream data show. We keep our tactical U.S. equity overweight yet watch for triggers for a change, such as earnings losing steam. We stay underweight long-term Treasuries. Even with the U.S. Treasury saying it aims to lower long-term yields, we see them rising anew as large fiscal deficits and persistent inflation cause investors to demand more compensation for the risk of holding bonds.

Evolving our fixed income views

Tariff risks reinforce our preference for euro area government bonds, so we go tactically overweight. U.S. President Donald Trump has signaled potential tariffs on Europe. Europe’s reliance on the U.S. as an export destination means tariffs – and any retaliation – would hurt euro area growth more than it boosts inflation, in our view. In the UK, we cut our gilt allocation to neutral. We had expected more Bank of England rate cuts than markets were pricing. Recent volatility, especially revived fiscal concerns, pushed yields to 17-year highs. Yields have since retreated as we expected, providing a better exit point. Markets have moved closer to our view on BOE policy rates – and we think concerns about the UK fiscal outlook will linger.

Emerging markets are especially vulnerable to the growth hit from tariffs and any worsening in global risk sentiment, we think. Mexico, with its heightened exposure to tariff impacts, is a key constituent in emerging market bond local currency indexes. We prefer to express heightened risks through fixed income, where we go underweight emerging market local currency debt. Tariff uncertainty could also drive volatility in currency markets and hurt returns in local currency EM debt.

Our bottom line

We stay overweight U.S. equities on a solid macro backdrop and the AI theme. We upgrade euro area government bonds, trim UK gilts to neutral and go underweight emerging market local currency debt.

Market backdrop

U.S. stocks were flat last week. Risk assets slid after the U.S. tariff plans before recovering by week’s end. Solid Q4 corporate earnings helped risk sentiment, with U.S. big tech companies reporting solid results and increasing their AI buildout spending. U.S. 10-year Treasury yields touched seven-week lows before settling near 4.50%. The U.S. jobs data showed a strong economy is keeping demand for workers high and leading to a renewed rise in wage pressures.

We get U.S. CPI for January this week. Even as December’s CPI report showed signs of inflation pressures easing, wage growth remains above the level that would allow inflation to recede back to the Federal Reserve’s 2% target, in our view. We see persistent services inflation forcing the Fed to keep rates higher for longer.

Week Ahead

Feb. 12: U.S. CPI

Feb. 13: UK GDP

Feb. 10-17: China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 10th February, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.