Wei Li – Global Chief Investment Strategist of BlackRock Investment Institute together with Carrie King –

Chief Investment Officer of U.S. and Developed Markets, Fundamental Equities, Carolina Martinez

Arevalo – Portfolio Strategist and Michel Dilmanian – Portfolio Strategist all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Broadening earnings: We think U.S. corporate earnings strength will keep broadening beyond tech in the Q3 season. We also see bright spots in Japan and European sectors.

Market backdrop: U.S. stocks ticked up last week to new record highs, powered by the ongoing rotation into small caps. U.S. 10-year Treasury yields hover near recent peaks.

Week ahead: This week, we eye euro area flash PMIs after the European Central Bank (ECB) cut interest rates for a third time. We think it will step up the pace of rate cuts.

U.S. stocks are hitting new highs – after a summer slump – as Q3 corporate earnings season kicks off. We prefer broad U.S. equities as we expect corporate earnings strength to keep broadening beyond tech. Federal Reserve rate cuts and solid economic activity underpin our U.S. view. We’re overweight Japanese stocks as earnings prove resilient to a stronger yen. Weak growth keeps us underweight European stocks overall, but we have favored sectors like financials.

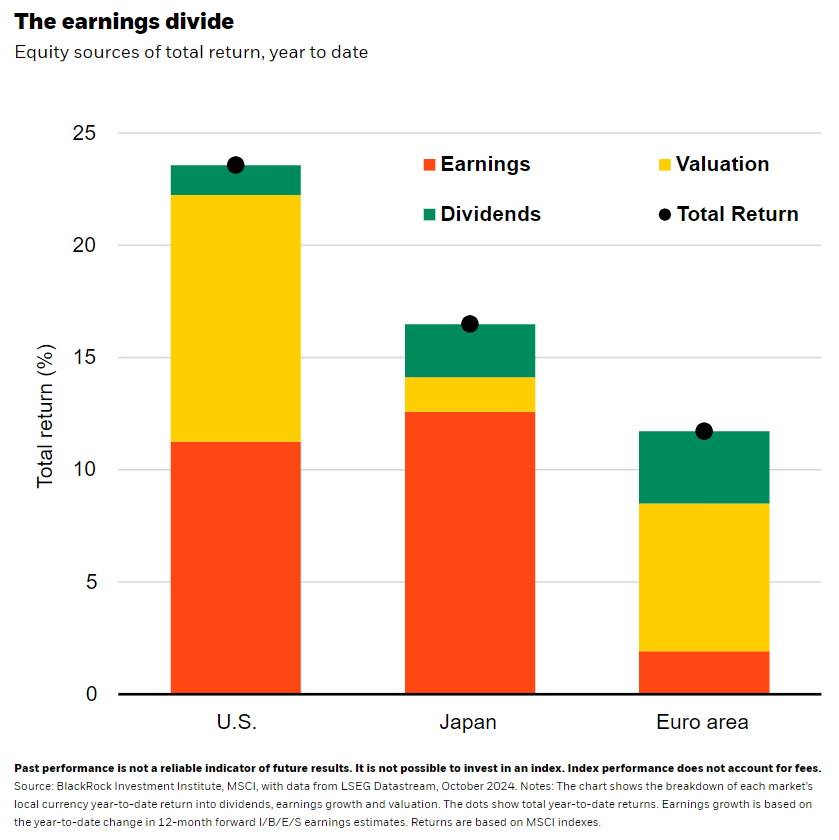

Favoring stocks over bonds has been rewarded this year as equities have climbed to new highs. Even as doubts over tech investment in artificial intelligence (AI) and recession fears stoked volatility, U.S. stocks have outperformed other regions this year on earnings growth and soaring tech valuations. See the chart. Jitters about lofty valuations and U.S. election uncertainty can drive market volatility. Yet on a six- to 12-month horizon, we stay overweight U.S. stocks as markets expect double-digit earnings growth over the next year and falling interest rates. We’re overweight Japanese stocks. Strong earnings growth that has boosted stock performance is slowing but remains resilient to a stronger yen. Europe’s story is slightly different: Earnings have been weak given poor economic growth. We’re underweight euro area stocks overall but see bright spots in sectors like financials and healthcare.

We prefer U.S. over European stocks. The reason: The near-term macro backdrop supports risk-taking in the U.S., even as markets have priced out some rate cuts. The Fed is cutting even as growth and the labor market hold up. We think earnings strength will keep expanding beyond tech, narrowing the gap between tech and other sectors. Earnings for a handful of top companies, mostly tech-related, are expected to grow 19% next year, down from about 30% in 2023 and 2024. Analysts see earnings for the rest of the S&P 500 growing 4% this year and 14% in 2025 after contracting last year, FactSet data show.

Our evolving AI views

We see ample room for the AI theme to run: Its buildout is only in the early stages. Yet investor doubts about tech spending on AI linger. We’ve expanded our AI preference beyond tech to sectors like utilities, energy, real estate and industrials. U.S. utility earnings have grown 8.2% over the past year, the fastest since 2020, based on LSEG data, partly due to AI’s big energy need. Utilities are neck-and-neck with tech as the best-performing sector this year. Our portfolio managers note that industrial companies tied to the AI buildout are seeing more demand than their peers.

Our global stock picks

Outside the U.S, we stay positive on Japanese stocks after trimming our overweight as a stronger yen drags on earnings. Solid wage growth, stronger corporate pricing power and shareholder-friendly reforms support earnings growth. Elsewhere in Asia, hopes for major fiscal stimulus have halted earnings downgrades for Chinese stocks. We’ve turned overweight Chinese stocks given this policy signal but that doesn’t change the long-term, structural challenges we are concerned about.

We stay underweight euro area stocks given weak growth and a limited recovery. Q3 earnings are expected to grow just 3.7% from a year earlier, with revenues still contracting. Yet we have favored outperforming sectors like financials. We also get granular in healthcare as some businesses will benefit more from AI and other mega forces, or structural shifts. We prefer European healthcare companies over their U.S. peers as they face less risk of losing revenue due to drug patents expiring.

Our bottom line

As Q3 earnings season gets underway, we stay overweight U.S. stocks and expect earnings to strengthen in sectors beyond tech. We’re also overweight Japan’s stocks. We’re underweight European equities but get selective in sectors.

Market backdrop

U.S. stocks ticked up last week to new record highs as Q3 earnings season kicked off. Small-cap stocks led the climb, cruising to their highest level since 2021. Tech stocks rallied to end the week after chipmaker TSMC’s sunny outlook hinted at robust demand for AI chips. U.S. 10-year Treasury yields ebbed to around 4.08%, just off recent highs but still up around 50 basis points in the past month. The ECB cut rates by 25 basis points for the third time this year and signaled a faster pace of cuts.

Global flash PMIs are on tap this week. In the euro area, recent weak PMIs point to contracting business activity. Slowing growth, weaker employment and inflation undershooting projections prompted the ECB to cut policy rates by 25 basis points again last week. Incoming data will be key for an ECB that has vowed to take a meeting-by-meeting approach on future policy decisions. Yet we don’t see the ECB returning to the old regime of very easy monetary policy.

Week Ahead

Oct. 23: Euro area consumer confidence

Oct. 24: Global flash PMIs

Oct. 25: U.S. durable goods; Tokyo CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 21st October, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.