Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Christian Olinger – Portfolio Strategist and Ann-Katrin Petersen – Chief Investment Strategist for Germany, Austria, Switzerland and Eastern Europe all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Election primer: We stay overweight U.S. stocks ahead of the election yet are cautious on bonds given the fiscal outlook. We focus on long-term positives in India and Mexico.

Market backdrop: U.S. stocks notched fresh highs last week and are up nearly 13% this year. The Bank of Canada and European Central Bank cut interest rates as most expected.

Week ahead: All eyes are on the Federal Reserve meeting this week. We see the Fed on hold in coming months even as other central banks start to trim policy rates.

Over half the world’s population goes to the polls in 2024. We watch for investment implications. We think governments and candidates have limited solutions to key financial issues for voters. We stay overweight U.S. stocks before the U.S. election yet cautious on long-term U.S. Treasuries. No matter who wins, budget deficits are set to stay large. Elections in India and Mexico sparked market volatility, but we focus on long-term positives. A July UK election supports our UK gilts preference.

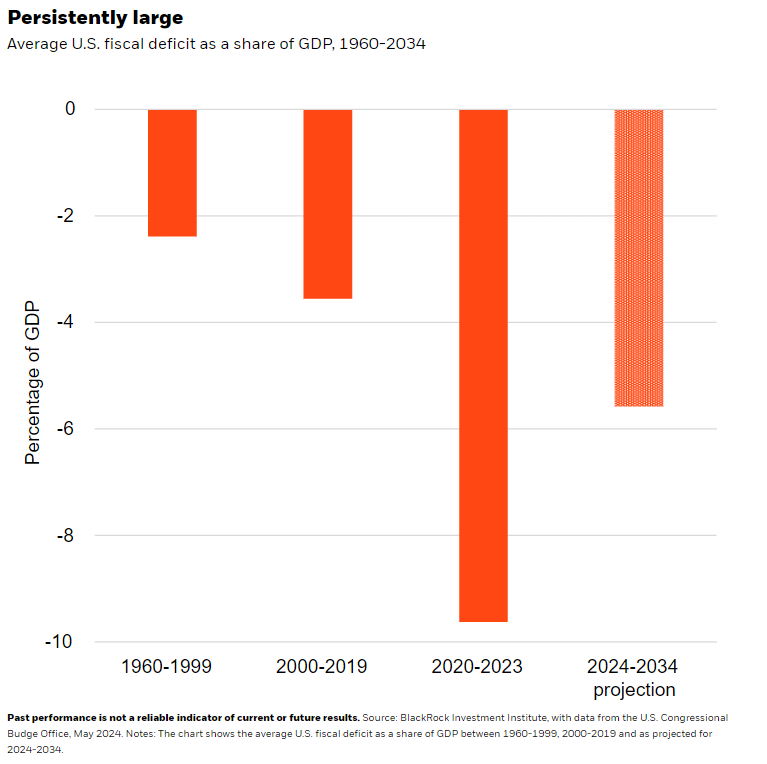

Global voters are expressing frustration about many issues but notably the rising cost of living. Yet we see many incumbent leaders or challengers constrained in any response, notably due to high public debt somewhat tying their hands. In November, U.S. President Joe Biden will face former President Donald Trump. Under both, pandemic borrowing swelled fiscal deficits – the shortfall in government revenue versus spending. No matter who wins, deficits are set to remain historically large. Neither is charting a path to a sustained reduction in deficits. See the chart. These deficits reinforce persistent inflation and our view that the Federal Reserve will need to keep rates high for longer. We think that, and markets needing to absorb large bond issuance, will spur investors to demand more term premium, or compensation for the risk of holding long-term U.S. bonds.

We track potential changes on U.S. trade, immigration and energy policy – and see a potential inflation boost no matter who wins. On trade, Trump has suggested a more protectionist stance that would levy a 10% across-the-board tariff and a 60% tariff on Chinese goods. Biden is expected to keep his current protectionist policies, like higher tariffs for some sectors, industrial policies favoring domestic production and the use of export controls. Major changes to legal immigration during a second Trump or Biden administration would have implications for inflation as the U.S. faces a shrinking working-age population. On energy policy, the Inflation Reduction Act (IRA) and its low-carbon transition investment incentives are in focus. If Republicans control Congress, they may revise or repeal parts of the IRA to fund tax cuts.

Elections around the globe

It’s already been a busy election year. In India, Prime Minister Narendra Modi secured a third term to lead the government but will need coalition support after failing to win a majority last week. That could slow some reforms – but it doesn’t change the long-term benefits from the confluence of mega forces, like a young population and digitalizing economy. Mexico’s election saw the ruling coalition score a resounding win that points to continuity. We see both India and Mexico benefiting from a rewiring of global supply chains. Though in Mexico, a new president and government rolling out broad reforms could weaken institutional checks and balances. Even as right-wing and populist parties performed well in the European Union elections, centrist parties are expected to keep overall control of the European Parliament. Yet the performance of governing parties will have repercussions, such as President Emmanuel Macron calling a snap election in France after his party suffered a big loss.

The UK votes in early July rather than in late 2024 as originally expected. A decisive victory for one party could create the political breathing space to address the UK’s structural issues, such as weak productivity growth. Beyond potential policy changes, a July election could allow the Bank of England to start cutting rates once it’s over – a reason why we like UK bonds.

Our bottom line

We stay overweight U.S. stocks for now and eye the key policy areas of the presidential election. On a strategic horizon of five years and longer, we like government bonds in the euro area and UK on expectations for lower interest rates.

Market backdrop

U.S. stocks notched fresh highs last week and are up nearly 13% this year. The Bank of Canada and the European Central Bank both cut rates for the first time since the start of pandemic. Markets are focused on how far central banks can cut rates – and are now split on whether the Fed will cut once or twice this year after the strong U.S. payroll gains last week. We don’t see these rate cuts as the start of a cycle of multiple cuts given sticky inflation holding above central bank targets.

All eyes are on the Fed policy meeting this week. We expect key data – like last week’s U.S. payrolls and this week’s U.S. CPI – to drive Fed decision-making. Even with easing likely on the horizon for the Fed and already underway elsewhere, this is not your typical rate-cutting cycle, in our view. The red-hot U.S. payroll data reinforces what an unusual environment this is for the start of a global easing cycle. We don’t see central banks cutting far and fast

Week Ahead

June 11: UK payroll data

June 12: Fed policy decision; U.S. CPI; UK GDP

June 14: U.S. trade data; University of Michigan consumer sentiment survey

June 10-17: China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 10th June, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.